The recent developments in the LPG market have been quite significant, especially in the eastern markets. This heightened interest is a direct response to the Panama Canal Authority’s (ACP) decision to limit the maximum number of transits to 31 from November 1st, owing to severe drought conditions. The impact of these restrictions, which are anticipated to persist until the conclusion of the dry season in May, coincides with Q4’s peak traffic season along the canal, indicating a prolonged effect on market dynamics.

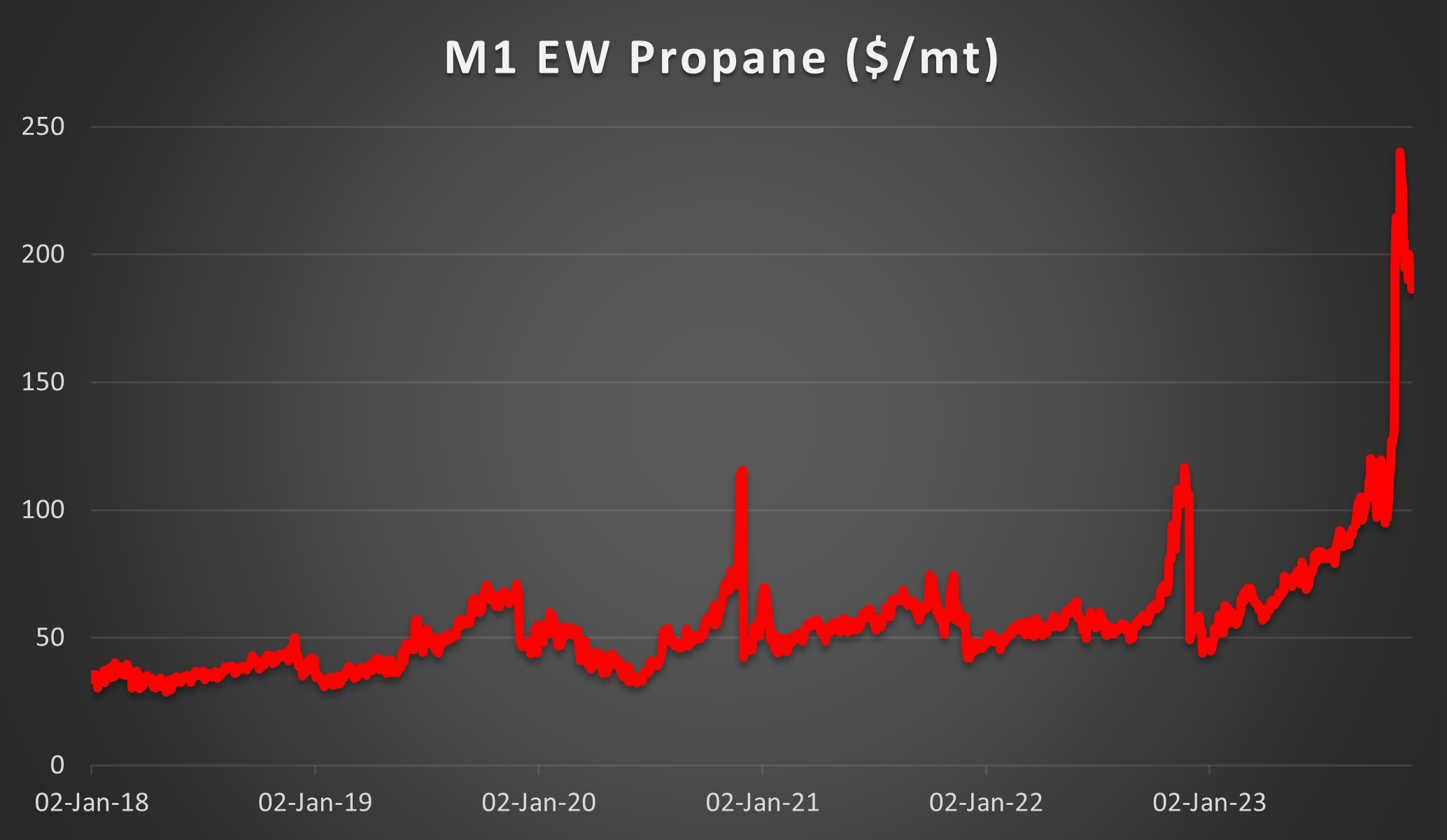

This situation has notably bolstered the FEI, culminating in the East/West reaching unprecedented levels. The December 2023 contract, for instance, surpassed the $240/mt mark, setting a new record for an M1 contract underscoring the significant implications of the transit limitations imposed by the ACP.

M1 EW propane from 2018

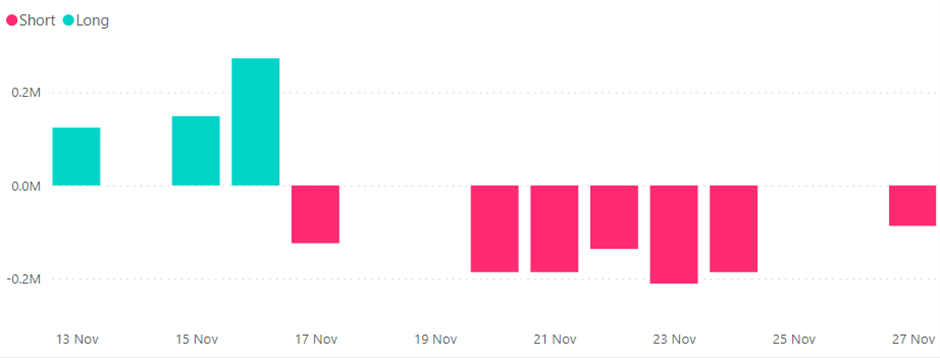

However, recently, there’s been a significant shift in the market behaviour of trade houses in FEI, as observed through the Onyx counterparty dashboard. Last week marked a notable change in their speculative flows, transitioning from a buying stance to selling. This shift is further highlighted by the Onyx COT dashboard, where the flow dynamics over the past seven days are now leaning more towards selling, exhibiting a 45:55 ratio on a long-to-short basis.

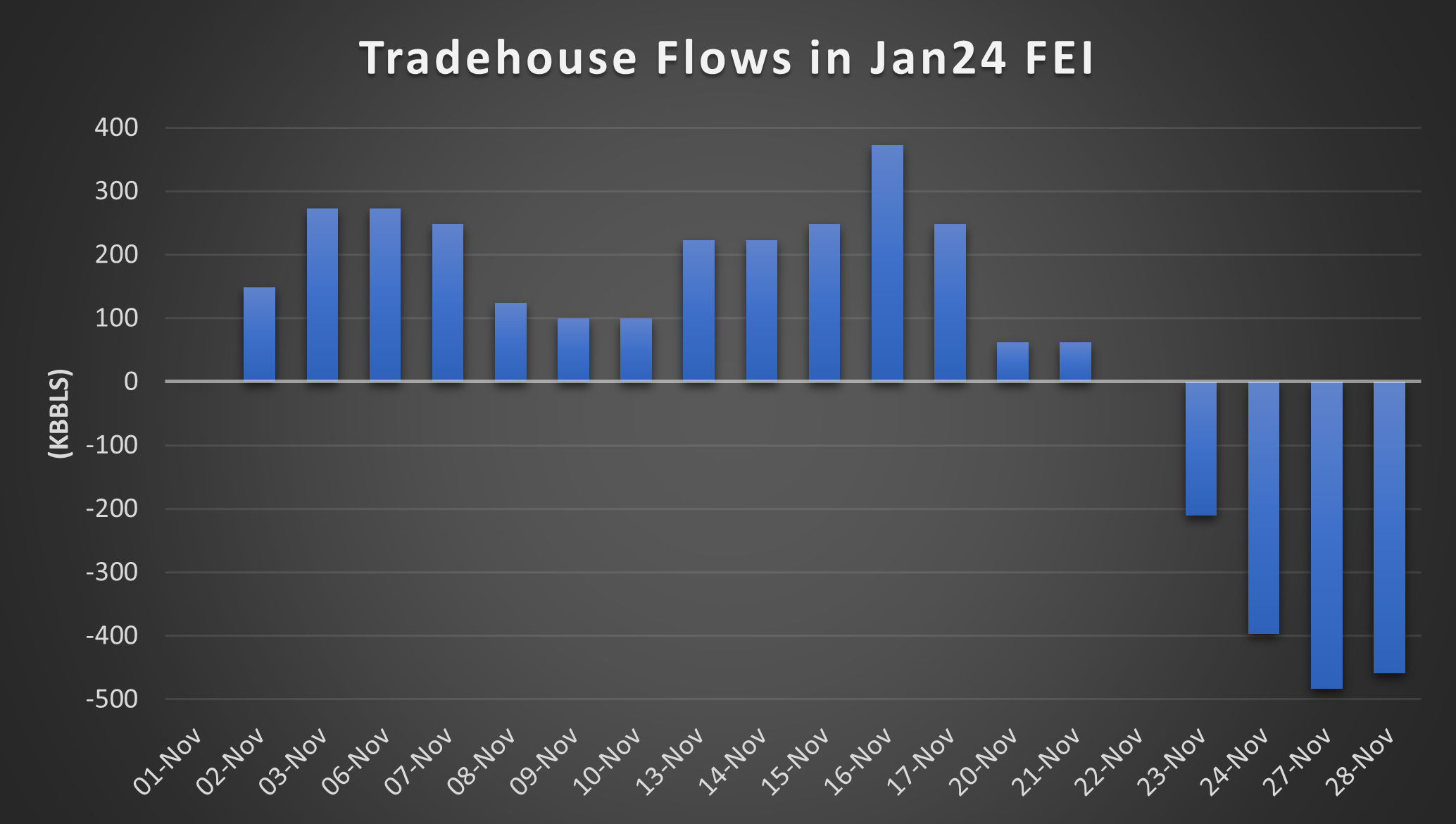

Tradehouse flows in Jan FEI from the beginning of November

Net flows in Jan FEI from November 13th.

This change in trading behaviour likely indicates a strategic move by these trade houses to take profit on their existing positions. Given the end of the year approaching, maintaining a balanced portfolio becomes a priority, and this shift towards selling can be viewed as an effort to realise gains from their previous long positions. Additionally, this strategy could also be a precautionary measure to safeguard against potential losses, aligning with a more cautious approach as the year draws to a close.

Conversely, in Europe, recent shifts in weather patterns have sparked an increase in heating demand, offering modest support to the market. As temperatures drop, several inland sources have reported challenges in procuring propane, attributing to a tightening supply that has pushed premiums higher. Contributing factors to this supply crunch include an escalated use of LPG in refineries, the spiking of LPG into natural gas, and an increased demand from the petrochemical industry. These elements are collectively reducing the availability of LPG at terminals.

Reflecting these market dynamics, the front EW has seen a retracement from its early month peak of around $240/mt to the current levels hovering at approximately $171.50/mt while Jan has shifted lower below the $170/mt handles.

December East/West Price Action.

January East/West Price Action

Freight dynamics have become a central focus in the market, and we are seeing adaptations by shippers due to the Panama Canal’s restricted vessel transit numbers. Many are opting for the Suez Canal route as an alternative to reach Asian markets. Initially, there was speculation that this shift might lead to increased flows towards Europe, potentially impacting the C3 NWE prices if these couldn’t be absorbed.

However, contrary to these expectations, such an effect on the C3 NWE prices has not materialised. Notably, we have seen trade houses selling the Jan EW contract with net selling of over 37kbbls between the 20th and 28th of November, which highlights how strength right now in Jan seems to be more concentrated in Europe.

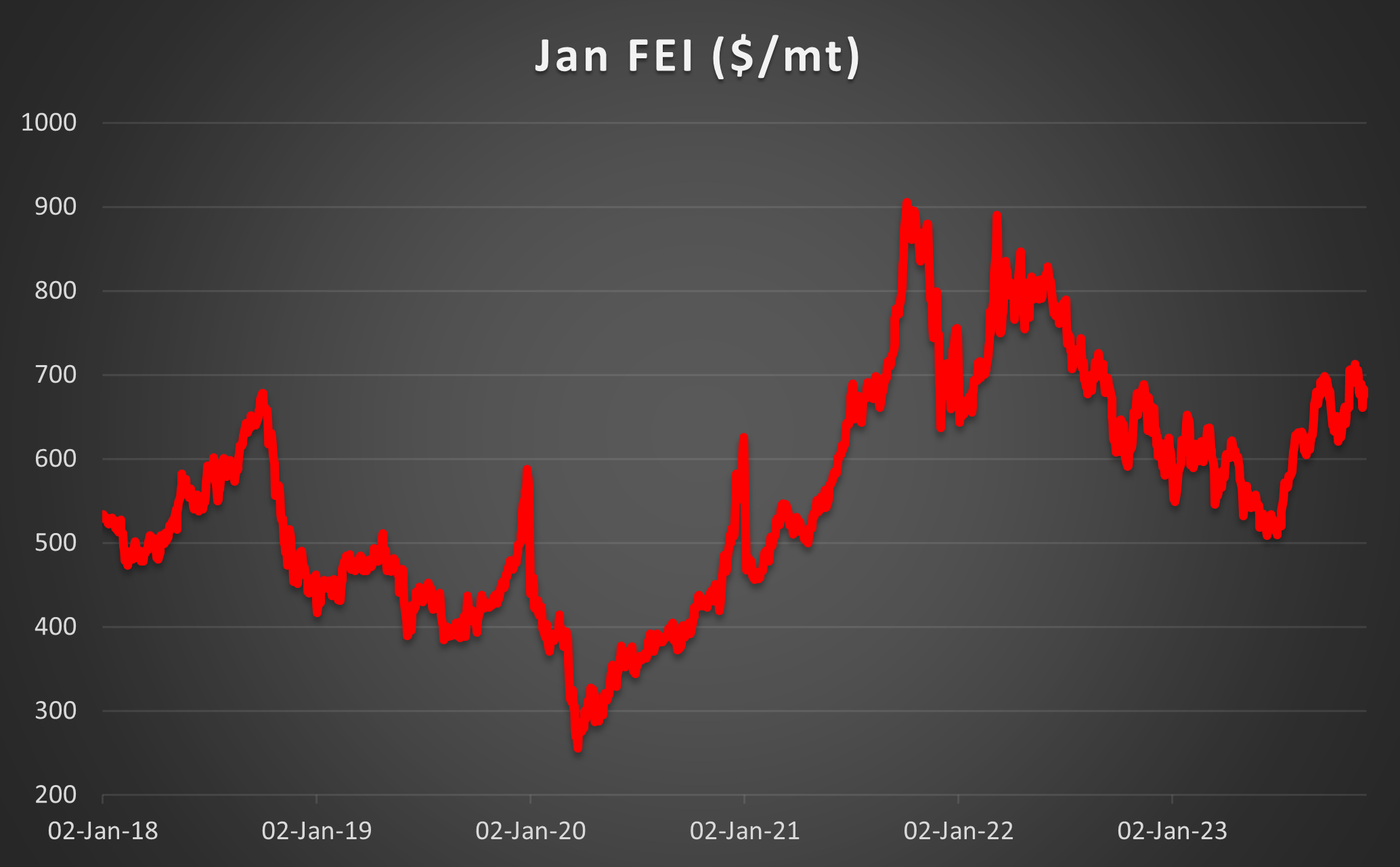

The delayed OPEC+ meeting will be key to watch though as further cuts to production could see the Middle Eastern market tighten and thus see supplies to the east limited, flaming renewed strength in FEI. On a flat price basis, the Jan FEI contract is still far below levels seen in 2021 and 2022 and so has not met psychological resistance yet so we will keep a close eye on new flows returning to the contract following the meeting on Thursday or if market participants continue with their more risk off mood.

January FEI Price Action.