To say the least, Q4 has been a volatile quarter so far for the gasoline complex, with prices for the crack spread seeing a U-shaped trend. Weakening US fundamentals on the back of increasing RINs supply was one of the catalysts for the crude flat price sell-off, with cracks falling to $3/bbl levels. Yet, the complex has proved resilient over November as the front-month EBOB crack rebounded to $9/bbl handles where it has remained supported. Amidst OPEC drama and weakening physical differentials for crude, a recovering gasoline complex may be one of the few saving graces for the crude market.

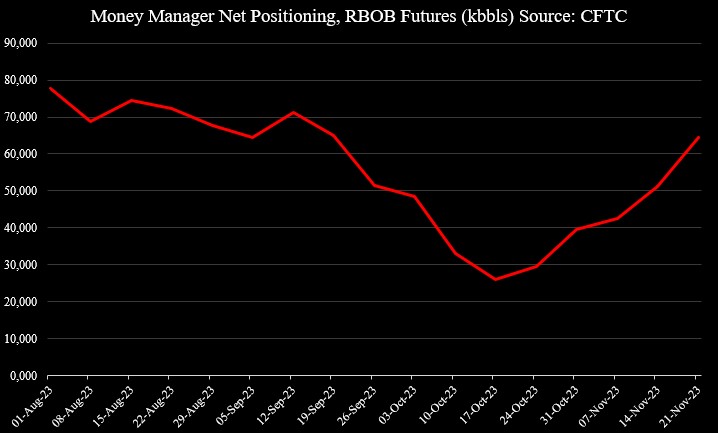

Money managers are certainly confident about gasoline and have continuously increased their bullish bets. In the week to Nov 21, long positions in RBOB futures are at their highest level since the end of September, which predates the last sell-off. Net positioning has increased for 5 consecutive weeks.

Despite bullish sentiment in the futures market, the arb (RBOB-EBOB) continues to trend lower, as a reflection of weakening US market against the European one on a relative value basis.

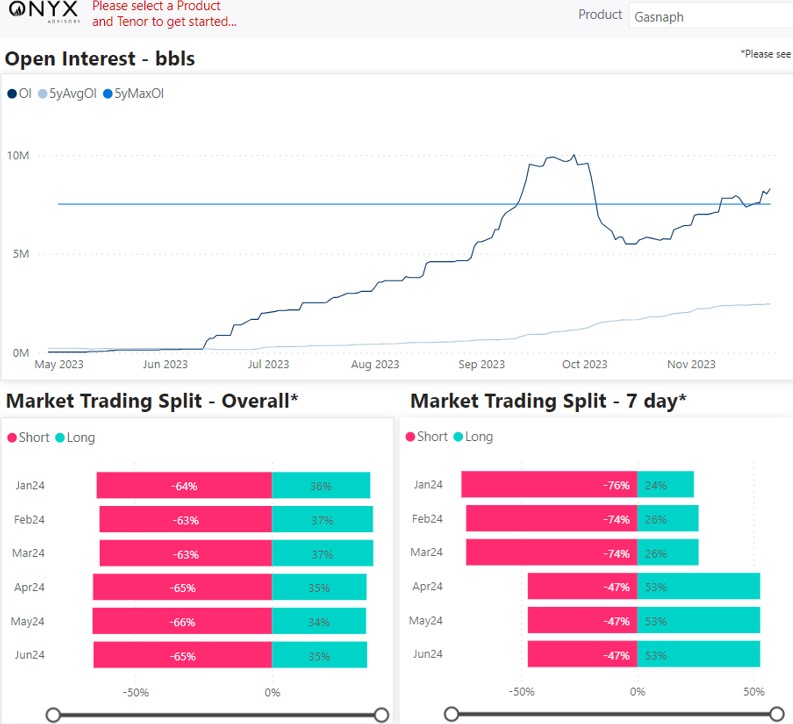

Now, gasoline is at a crossroads, and since Thanksgiving the market has been lacking inspiration and direction. There may be a ceiling to the recent rally, and this is quite poignant in the gasnaph (EBOB -NWE Naphtha) contract, with the December contract capped at $120/mt and seeing serious sell-side hedging flows at these levels. Open interest in Q1’24 tenors is steadily increasing with recent market participants positioned on the sell-side.

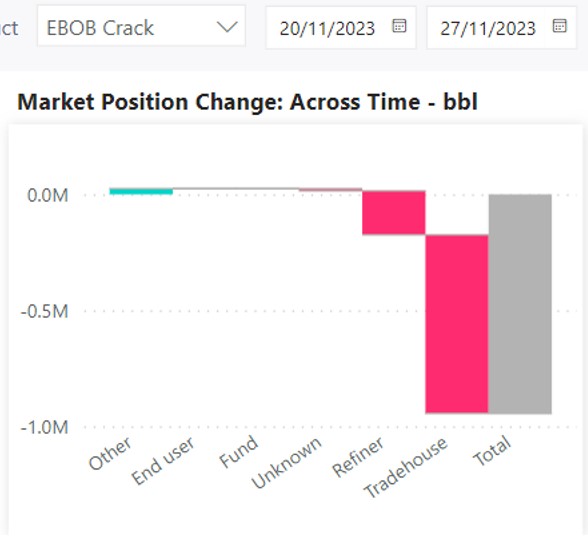

The pressure in gasnaph is thereby supporting the naphtha complex as cracks and spreads have rallied on stronger fundamentals, paper flows, and weaker crude. The Q1 EBOB crack has also encountered selling flows from refiners and trade houses, as indicated from our counterparty dashboard.

Meanwhile, the Dec/Jan EBOB spread has met resistance before the double-digit level, seemingly unable to breach this point.

As such, these paper flows suggest that the recent EBOB rally is reaching a plateau, with a significant volume of sell-side flow coming from refiners. Previously stopped-out length had returned and have also been well rewarded, but perhaps it is time to call it a day and take profit.

Despite gasoline prices meeting technical resistance, there is reason to remain optimistic, as cracks and spreads have returned to pre-sell-off levels and are elevated on a relative value basis. Just like how gasoline weakness was a factor in driving crude weakness, recent strength could see the opposite happen.

Although European refinery margins have been mostly supported from weaker crude, gasoline has held its weight. The M1 European refinery margin has increased from $3.10/bbl on Oct 31 to $7.26/bbl on 28 Nov, a significant rebound.

The light ends complex has staged an earnest recovery from October lows, and this could be one of the few factors supporting crude demand in the near-term. Furthermore, refineries typically buy crude in January as they top up inventories from seasonally low levels in December.

In a world of overwhelmingly bearish narratives for crude with OPEC caught between a rock and a hard place, stronger refinery margins and a resurgent light ends complex may prove to be one of the few bright spots for the brave bulls that remain.