The strength seen last week has continued, with May Brent futures starting the week in the $84/bbl handles, marking a 2.3% increase week-on-week.

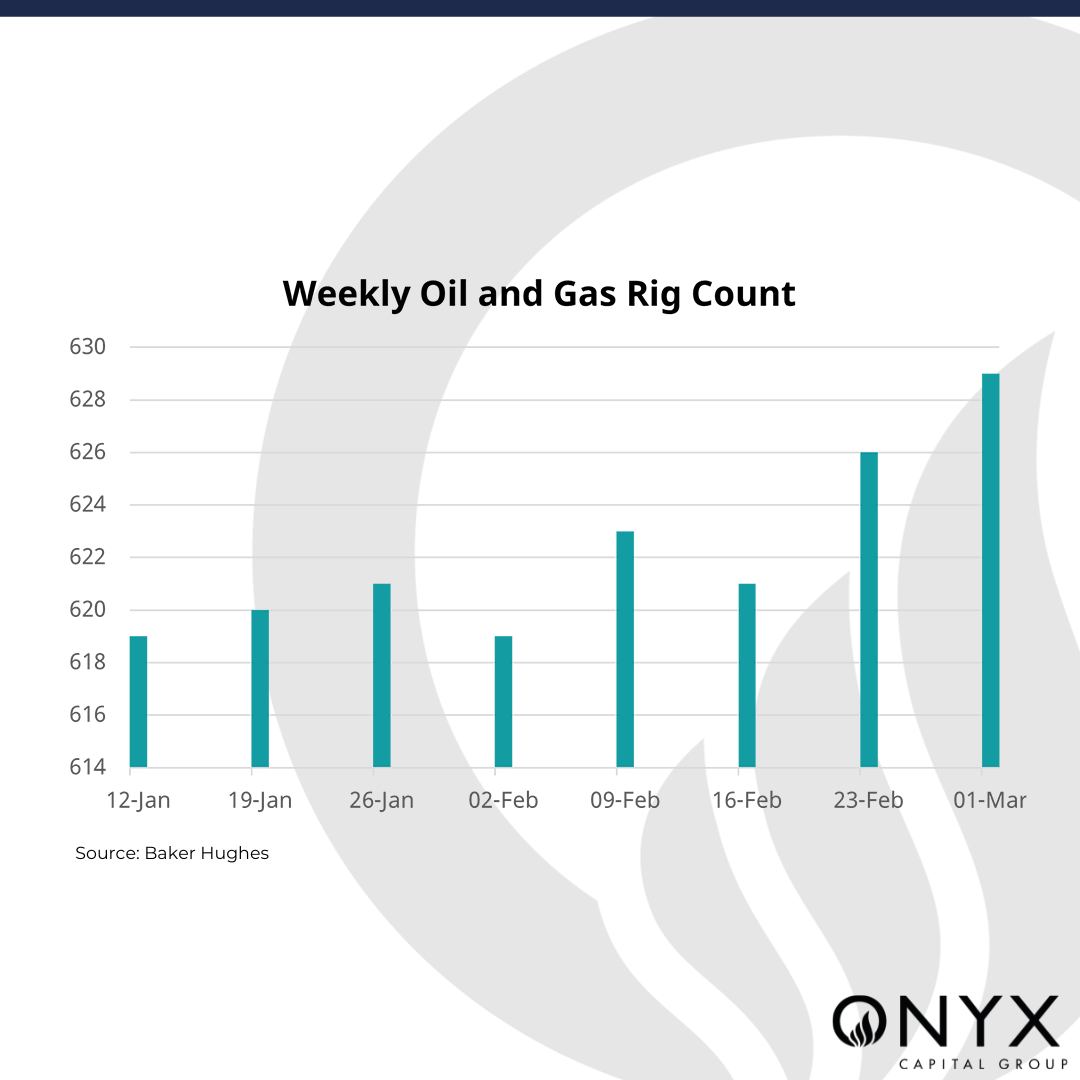

On 03 Mar, OPEC+ members agreed to extend its voluntary oil output cuts of 2.2mbbls/d into Q2’24, falling in line with analyst expectations. Saudi Arabia – a key component of the reduction – has vowed to extend its voluntary cut of 1mbbls/d through to the end of June, leaving the nation’s output at around 9mbbls/d. Moreover, according to Baker Hughes, the oil and gas rig count rose by three to reach 629 in the week to Mar 01, marking a second consecutive increase in rig count as players are looking to drill more, in line with the relatively higher oil prices.

Looking ahead to this week, the market remains very balanced, in a somewhat equilibrium state. Despite chaining together five days of growth in regards to prices, the strength has been seen without a great deal of volatility, with prices last week all settling around the $83.50/bbl mark. Therefore, with the OPEC+ news already priced in, we forecast a rather neutral view, predicting prices to continue to print in the $83/bbl handles. It will be important to keep a keen eye on any macro headlines or shocks which could spark some life and meaningful direction into the contract.