In our futures report on Monday, we highlighted our neutral-to-bearish view on the state of Brent futures for the week to Jan 12, quantifying this with a forecast that prices will sit around $75-77/bbl at the end of the week. On that note, while prices were largely trading slightly upwards of this range, between the levels of $76-78/bbl, they surged into $80 territory on Jan 12 and currently (as of 16:45 GMT) sit at $78.60/bbl.

The initial view emerged on the back of expectations of the narratives of weak global oil demand having a small edge over bullishness from news on Libya’s NOC declaring a force majeure at its largest oil field. In addition, our view was well supported by bearish EIA stats announcing a US crude stocks build of 1.338mbbls (against forecasts of a small draw) in the week to Jan 05. Mar Brent futures fell from $78/bbl two hours before the stats were announced to $76.59/bbl by 18:50 GMT on Jan 10. This bearishness was further fuelled by builds in gasoline stocks (at +8.03mbbls against estimates of +2.13mbbls) and distillates (+6.528mbbls against an estimated +1.76mbbls).

Notwithstanding this, prompt Brent prices ultimately strengthened on account of air and sea strikes conducted by the United States and Britain on several sites used by Houthi rebels in Yemen in response to the Houthis attacking ships in the Red Sea. The air strikes resurrected concerns about an escalation of the conflict in the Middle East and the larger impact this could have on oil supply, especially those flowing through key choke points like the Strait of Hormuz. While these critical chokepoints remain free of disruptions as of yet, these fears could continue to place a premium on Brent prices.

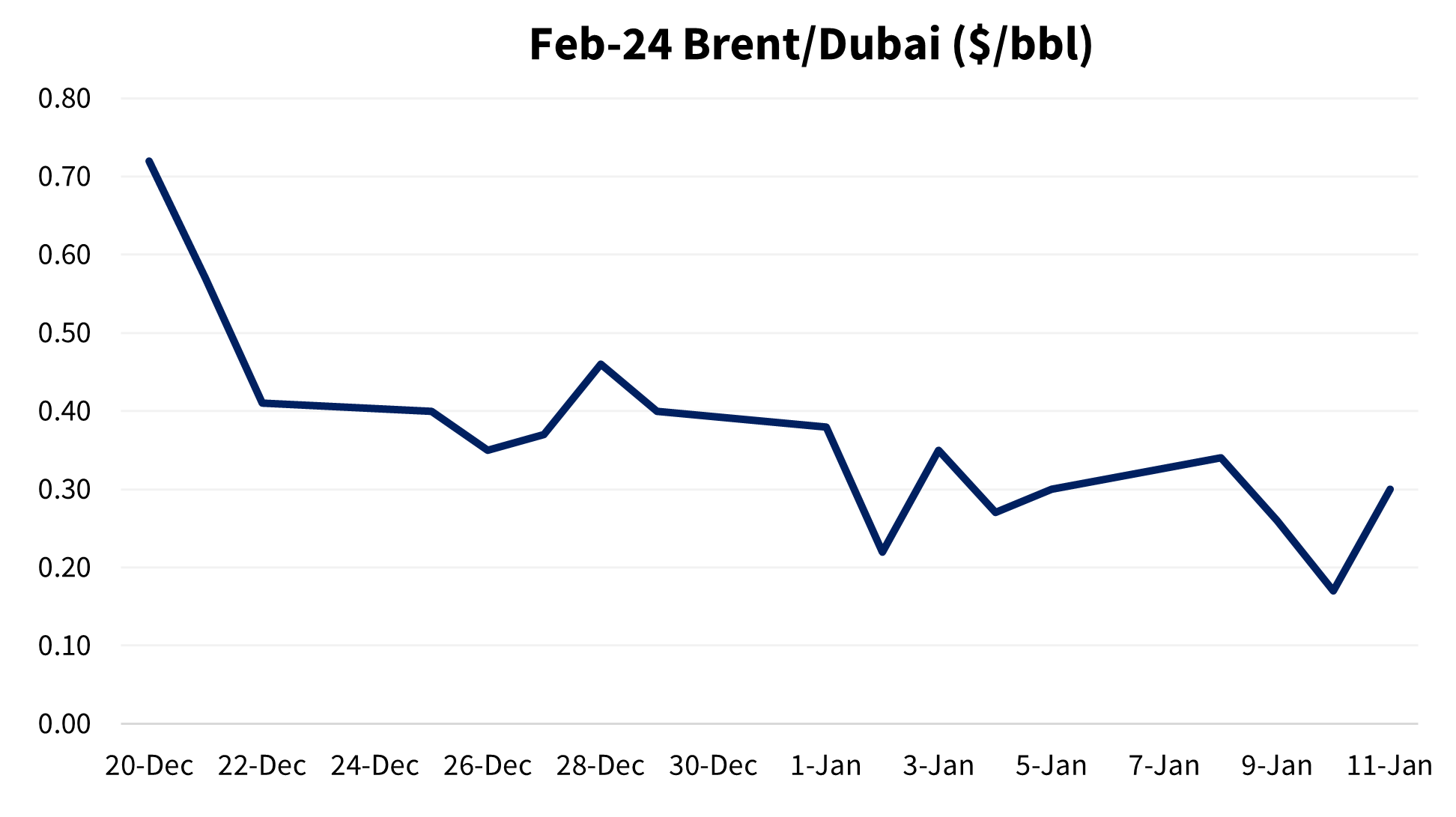

It will be interesting to observe whether we will observe a rise in volatility in the coming week or if market behaviour will neutralise instead. We find support for the latter viewpoint in Brent/Dubai. An escalation in the war in the Middle East would ordinarily contribute to Dubai crude rising by more than Brent. However, with the limited reaction in Dubai crude and with the prompt Brent/Dubai rising from $0.17/bbl on Jan 10 to trading around $0.60/bbl on Jan 12, we find ourselves wondering about the robustness of the geopolitical risk premium on Brent.

Finally, amid news such as Citigroup lowering their Brent price forecast for 2024 by $1 to $74/bbl and their 2025 forecast by $10 to $60/bbl citing oversupply concerns, it will be pivotal to understand this see-saw between bearish fundamentals and risk premia