Manchester United – Brent Futures

Despite Liverpool surpassing Manchester United to become the most decorated football club in England, on the back of winning the domestic cup double of both the FA Cup and the less prestigious English League Cup in the 2021/22 season, Manchester United still remain the King of the modern Premier League, having won the title 13 times, with the next best being their local rivals, Manchester City with 7. Roy Keane recently hammered home this point following a goalless draw at Anfield, reminding Liverpool defender Virgil van Dijk that “he’s playing for a club [Liverpool] who have won one title in 30-odd years”. Thus, there was only one team that could reflect Brent futures.

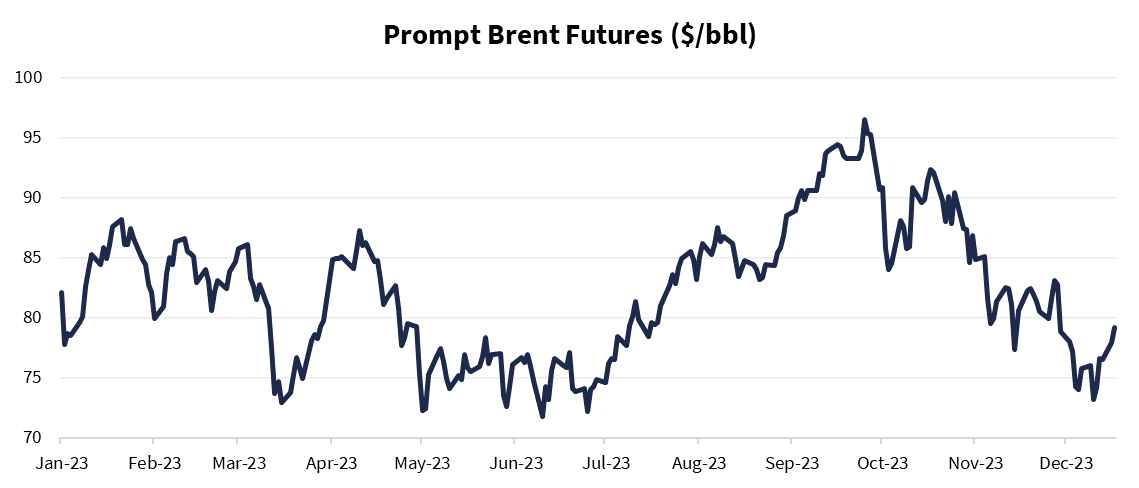

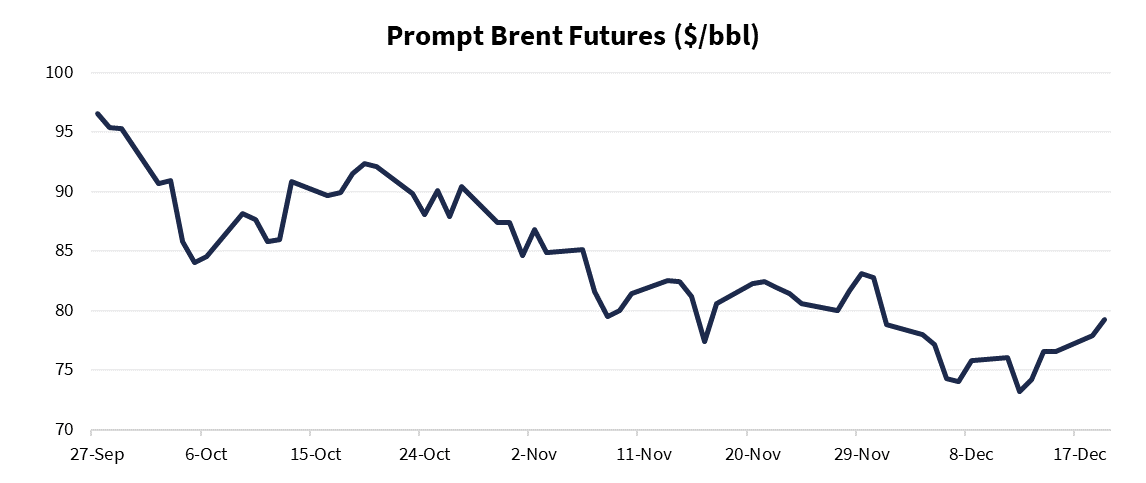

The rolling prompt month Brent Futures has seen a topsy-turvy year to say the least. A surge was seen in Q3, with the majority of the leg work done in September, with price action rising from $74.65/bbl on July 03 to achieve a closing price peak of $96.55/bbl on Sep 27. OPEC remained the ‘puppet master’, much like a flashback to Sir Alex Ferguson’s magnificent tenure at the club, with Saudi Arabia and Russia being key players, having removed over 125mbbls from the market over the quarter, helping to bolster this rally towards triple digits.

However, much like the managers who were faced with succeeding the ‘Fergie’ era – none of whom have been able to repeat the same success, including the latest victim in the form of Erik Ten Hag – this height reached by the prompt Brent futures was indeed the peak, in turn price action has been seen tumbling down the hill in the closing months of 2023.

As the $100/bbl mark got to near touching distance, a long-saturated market who had already withstood the great temptation of cashing in a week prior, when prices rose to above $94/bbl, had to look themselves in the mirror once again and ask whether it could get much better. Inevitably the answer was no! Spurred by signs of weaker gasoline demand, the market reacted in force and a flurry of profit-taking saw price action decline by over $10/bbl in a single week, falling to $84.07/bbl come Oct 05.

Although, just as things started to look bleak for Brent, the first of two prominent conflicts in Q4 begun, with Isarel-Hamas the early kick off on Oct 07. Prices were buoyed by the geopolitical risk premium emanating from an escalation in attacks, with Israel likely looking to initiate its ground offensive, placing a crucial chokepoint, the Strait of Hormuz, in increased danger of closing. As a consequence, market participants, speculators and physical hedgers alike looked to increase their length, sending prices back northwards of the $90/bbl mark, summitting at $92.38/bbl on Oct 19.

In a good see-saw action, prices retreated down as Brent flat price saw a muted reaction to further developments. After grinding lower for three weeks the psychological $80/bbl resistance level was finally subducted on close of Nov 08. Bearish sentiment was fuelled by poor economic data from China, driving concerns about the energy demand outlook in the Far East, coupled with weaker Asian refinery margins. Brent futures finally reached contango on Nov 17.

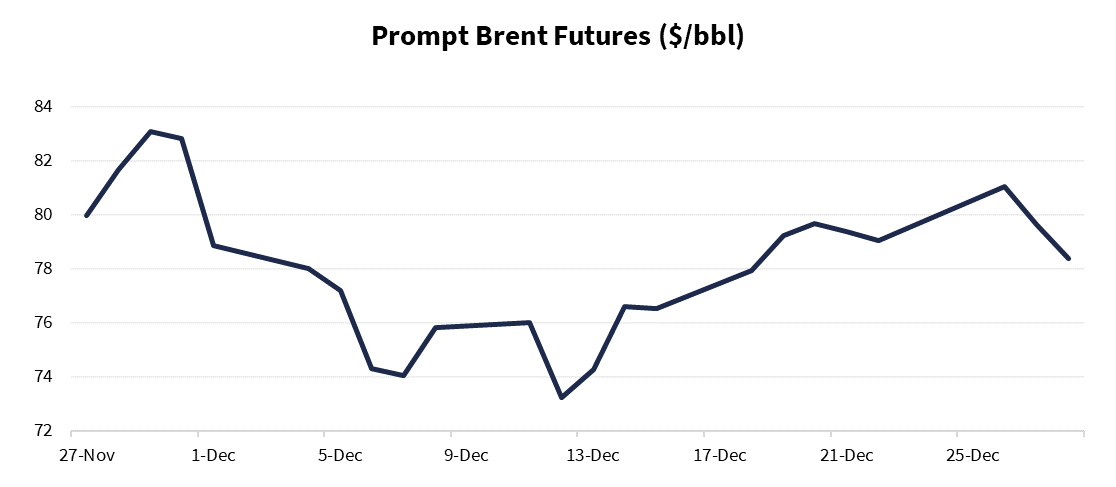

Fast forward to the end of the month and OPEC was back to playing its fiddle. A delayed OPEC+ ministerial meeting saw prices being supported from $79.98/bbl on Nov 27 to $82.83/bbl come Nov 30. However, in the week following the Nov 30 meeting and with the outcomes finalised, price action plunged to below the $75/bbl mark on the back of traders being left very unimpressed, a feeling Manchester United fans have become all too familiar with this calendar year.

As we closed 2023, there was enough added time for the second of the major conflicts, with Yemeni Houthi rebels launching attacks on commercial vessels transiting the Red Sea, as an act of revenge against Israel for its military campaign in Gaza. This again helped to bolster prices, rising from the $73.24/bbl dip on Dec 12 to above the $80/bbl mark come Boxing Day. However, as tensions seemingly simmered into year end, alongside reports of Chinese and Russian ships not being targeted and allowed to freely move throughout the Suez Canal, the geopolitical risk premium collapsed and prices decreased accordingly.

Manchester United has likewise had a year full of highs and lows, from winning the League Cup in February to finishing bottom of their Champions league group come December. Currently sitting 8th in the Premier League, equidistance between top and relegation on a points basis, it is all to play for in the two competitions remaining for the ‘Red Devils’ in the 2023/24 season; much like Brent futures as we enter 2024.

Arsenal – Naphtha E/W

Arsenal last won the Premier League 20 years ago in their ‘Invincible’ 2003/04 season. Last season they got to within touching distance of the title, however, after surging 8 points clear at the top of the table on Mar 19, a tough run in April saw the Gunners drop 9 points and have their title hopes all but disappear.

This falls in line with ten consecutive days of declines in the Q1’24 tenor for Naphtha E/W, falling from highs of $6.25/mt on Mar 15 to close negative at -$1.50/mt on Mar 28. This occurred on the back of physical selling in the prompt MOPJ flat price, as a consequence of weaker cracker run rates and poor petrochemical demand. In turn, February 2023 recorded the lowest number of Japanese imports of Naphtha in 14 years. Q1’24 Naphtha E/W price action found a floor at -$3.50/mt on opening of Apr 04 before the E/W saw buying confidence emerge from, MOC bidding, some short covering and bullish interest in MOPJ spreads at these lower levels.

After last year’s failures, Arsenal will be looking to have their red and white ribbons on the trophy come May 2024. They have started off the season well, sitting in pole position at the top of the tree on Christmas Day after recording an impressive 2-0 victory over Brighton on Dec 17. Although, three games without a win, including two losses to West Ham and Fulham, optimism has started to wane into the New Year, with the Gunners now down to 4th and only one point ahead of their fierce North London rivals, Tottenham Hotspur.

In a similar vein, Jan Naphtha E/W has seen a volatile last couple of weeks. The prompt contract was initially supported, rising from lows of $11.75/mt on Dec 05 to above $30/mt come Dec 18, on the back of bullish signals. Firstly, due to bad weather and poorer exports out of Russia, Black Sea FOB negotiations never materialised, meaning that the expectation of large sell side hedging flows, which the market had already started to price in through heavily offering the Jan E/W to below $12/bbl-handles, were taken out, leaving room for the contract to surge. Deferred E/W saw buying interest out of FEI/MOPJ selling, lending further support to the prompt.

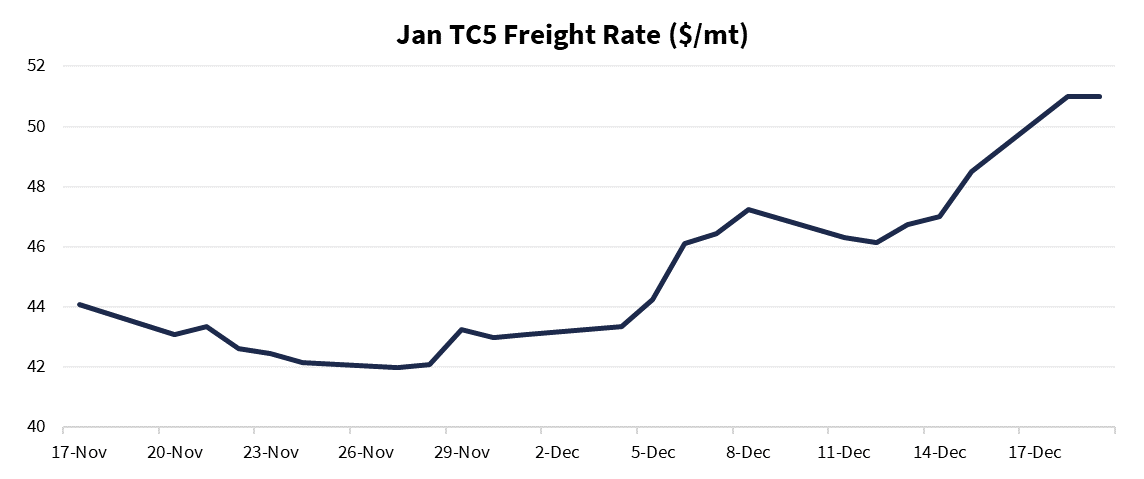

Moreover, Dec TC5 was heavily shorted going into December pricing, down to WS145, as a consequence of players expecting less naphtha supply due to AG maintenance, thus, weakening demand for vessels to move product to the East. However, once players caught wind of the news that some major shipping companies would suspend transit through the Red Sea, due to the escalation of attacks from Yemen-based Houthis on commercial vessels, freight rates began to roof. Bal-Dec rose to highs of WS175 and Jan TC5 surged almost $10/mt since the start of the month to $51/mt on Dec 19. Subsequently, naphtha E/W gapped up.

Although, a significant portion of this rally happened before the news was officially released, hinting at players acting on rumours. Therefore, when the news hit the public on Dec 14 and even after escalation over the weekend, reaction was limited and the E/W did not perform, with these bullish signals having likely already been priced in. Conversely, prices retraced as buying interest ceased and players began to sell the news, alongside increased security surrounding the Red Sea attacks, reducing the risk premium. Thus, the prompt E/W fell back down to $25.25/mt on Dec 20 and then $19.00/mt come Dec 22.

Arsenal will be hoping that this retracement will not be further seen in their performances, as they aim to go one place better this time around.

Aston Villa – 0.5% Barge Crack

Former Arsenal boss, Unai Emery, has been Aston Villa manager for a little over a year now. Since his appointment, Aston Villa have gone from relegation candidates to potential title contenders, sitting one point below the leaders as of Dec 22. In regards to fuel oil, 0.5% Barge crack has seen a strong 2023, with the Q1’24 contract rising from lows of -$2.80/bbl on Jan 04 to highs of $3.89/bbl come Dec 19, still patiently waiting to surpass the $4/bbl barrier.

After a poor start to the season, notably opening their campaign with a 5-1 defeat away to Newcastle, Aston Villa have seen a resurgence, recording back-to-back 1-0 victories against Manchester City and Arsenal at the beginning of December. Likewise, 0.5% Barge crack has seen support, with the 8-day moving average surpassing the 21-day on Nov 02, a strong bullish indicator, alongside both moving averages travelling on near-continuous uptrends since Oct 27 and Nov 07, respectively.

Resilience and stability have been two words closely associated with 0.5% Barge crack over the past few weeks. Resilient in the front, on the back of a strong physical market, with scale-back spread buying and deferred Euro crack buying. Moreover, stability has been portrayed through prices remaining at elevated levels and continuing to keep climbing, piling the pressure on the Q1’24 0.5 E/W. This was especially evident in H2 Nov and H1 Dec, where price action fell over $10/mt from $50.39/mt on Nov 20 to close below the $40/mt come Dec 07.

Chelsea – Q1’24 Gasoline Arb

As Chelsea Football Club embarked on their first full year under new American ownership, in the form of Todd Boehly, results did not align with the $1bn spent since the takeover in May 2022. In a similar vein, the transatlantic gasoline arb has seen a weak year, with the Q1’24 contract falling over 20c/gal since the start of the year to 11.73c/gal at close on Dec 12.

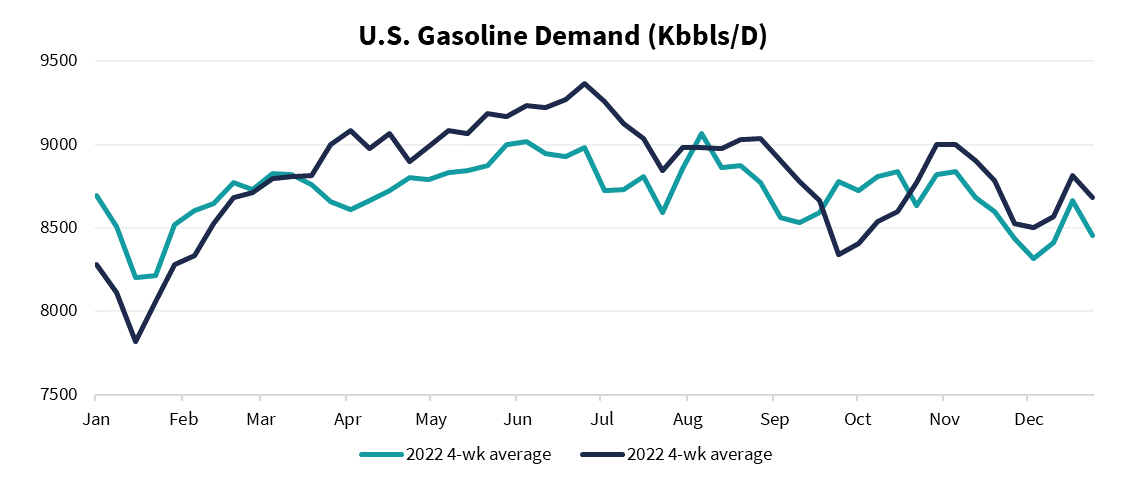

Notable weakness was seen towards the end of September, with US gasoline demand, in terms of 4-week average, plummeting from above 9.0mbbls/d to below 8.5mbbls/d, subducting the 2022 4-week average for that time period in the process. Alongside this, a more bullish European structure saw the Arb get ‘hit for 6’, with Q1’24 coming off from 22.14c/gal on Sep 19 to 17.33c/gal come close on Sep 22.

However, similar to Chelsea recording back-to-back home wins on Dec 17 for the first time since Oct’22, the Arb has seen recent support, chaining together six days of consecutive growth, taking the prompt to 7.80c/gal on Dec 20, with 8c/gal acting as an apparent psychological barrier.

Everton – LST/FEI

Everton Football Club have been on a downward spiral for the past couple of seasons, narrowly avoiding relegation over the course, to remain one of six teams to have never been relegated from the premier league. Although there’s no relegation to worry about when it comes to oil derivatives, the LST/FEI Arb has had a year to forget in terms of price action. The Q1’24 LST/FEI has seen a seismic fall of almost $200/mt, from -$115/mt-handles in the opening days of 2023 to lows of -$348.34/mt on Nov 09.

This low was seen on the back of nearly three weeks of continuous declines, fuelled by Panama Canal restrictions due to low water levels, rallying freight and a Force Majeure declared in many terminals in the US. As a consequence, Q1’24 price action fell by over $115/mt across the 17 trading day period, from Oct 17 to Nov 09. Comparably, Everton were deducted 10 points on Nov 17 on the account of breaching Financial Fair Play rules, sinking them to bottom of the Premier League.

However, more often than not, what goes down must come back up. Alongside a resurgence in Everton’s performances, with ‘Dyche-ball’ in full swing, the LST/FEI Arb has also seen some much-needed support, initially attributed to weaker freight and poorer Asian demand.

LST flat price then began to strengthen, lending support to the Arb, in spite of several cargoes being cancelled out of the US, leaving a potential supply overhang. This was partially credited to notable stock draws over the prior weeks and higher exports, with 44% of US cargoes still moving through the Panama Canal, a much greater figure than what was expected. Yet, the most significant factor was short coverings and Jan LST buy backs from funds and majors, providing LST with ‘synthetic’ strength. Subsequently, when said funds and majors terminated their short covering and the bull LST play came to an end, the Q1’24 Arb felt the pressure and retraced lower back to -$320/mt-handles. Everton will be hoping their recent recovery is far more set in stone as they enter the New Year.

Post Match Analysis

As we enter the second half of the season and a new calendar year there will be some key indicators to watch out for in the market. OPEC+ has generally been the most decisive factor across 2023, however, with waning crude oil demand the threat of cuts has lost its star power in recent times. Refinery margins will become increasingly important to monitor, in combination with OPEC announcements, to ensure an accurate projection for the crude price, with global geopolitical imbalance ready to add fuel to the fire. Chinese quotas and Asian demand also provide a key factor looking into 2024, with olefin demand a particular focus for the lightends market. Finally, freight will continue to be of great interest, as it looks to infer the open or closed status of arbs across the globe. Nevertheless, no matter how much analysis you do on paper, it is the players on the pitch who make the difference – who will win the 2024 Ballon d’Oil?