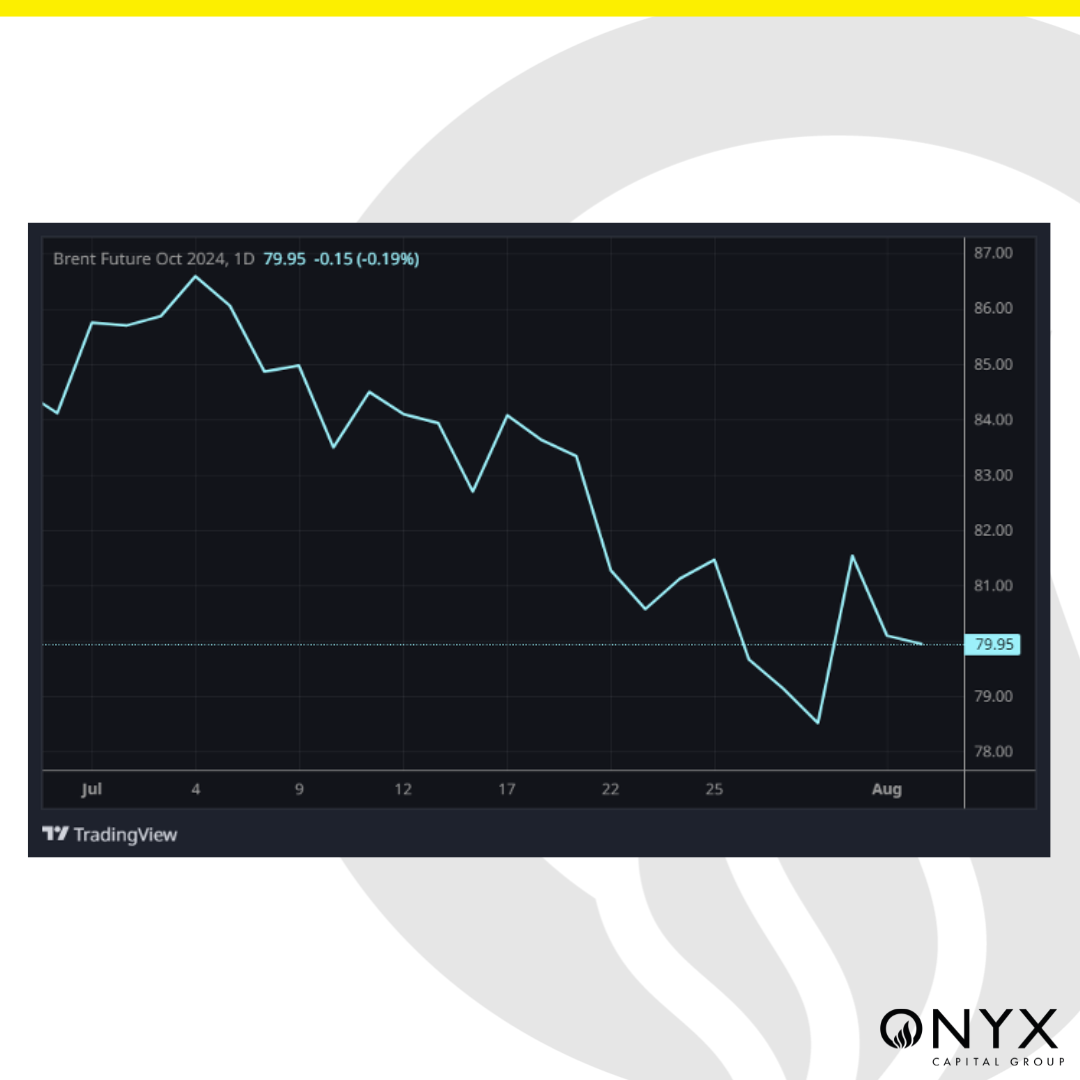

We expected the now-prompt October’24 Brent futures contract to trade between $78-80/bbl at the end of the week. In line with this forecast, the benchmark futures contract sits at $79.90/bbl as of 10:00 BST on Friday. As we recap what was a significant week for sentiment amid the Sep’24 Brent expiry on Wednesday and a slew of macroeconomic data through the week, we find three factors pivotal in impacting the futures this week:

- Sell-off in Brent spreads

- EIA statistics for the week ending 26 July

- Macroeconomic data

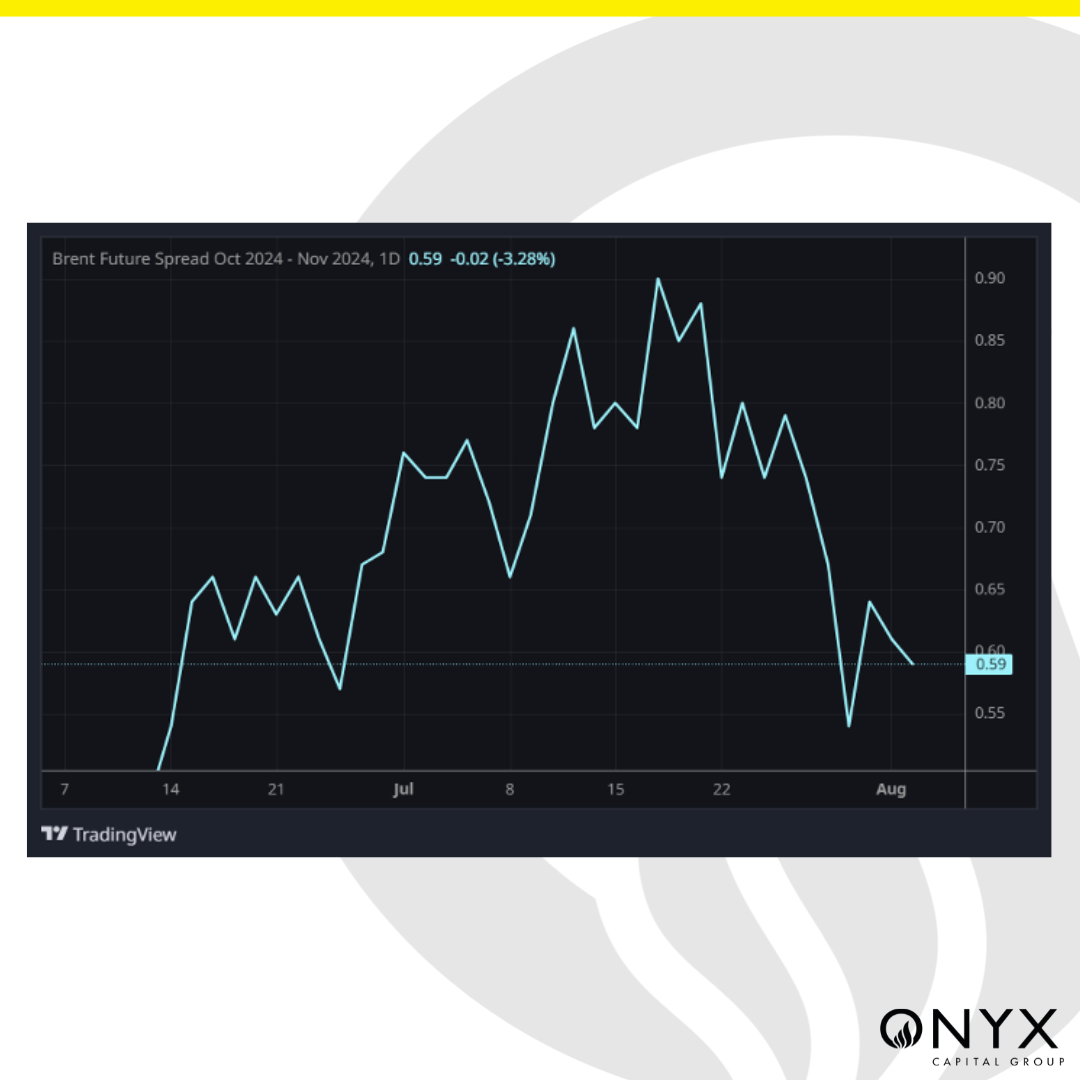

The Oct’24 Brent futures began the week on a bearish foot, settling at $79.10/bbl on Monday and then inched lower to $78.50/bbl the following day. The Oct/Nov’24 Brent futures time spread, however, collapsed from nearly $0.70/bbl on Monday to $0.55/bbl the next day. This sell-off in Brent spreads was pivotal in defining the weak sentiment in the futures contract, especially since the Oct/Nov spread was holding up around $0.80-0.90/bbl in previous weeks despite a weaker flat price. Considering the downward trajectory observed, this spread selling may have also been exacerbated by length stopping out. We subsequently saw a small recovery the next day, amid the Sep’24 Brent futures expiry. Trafigura offered two Midland cargoes in 31 July’s physical window, 21c above the implied curve, which were lifted by Equinor. Amid these drivers, the Oct’24 Brent futures contract rallied to $81.55/bbl, where it closed on 31 July.

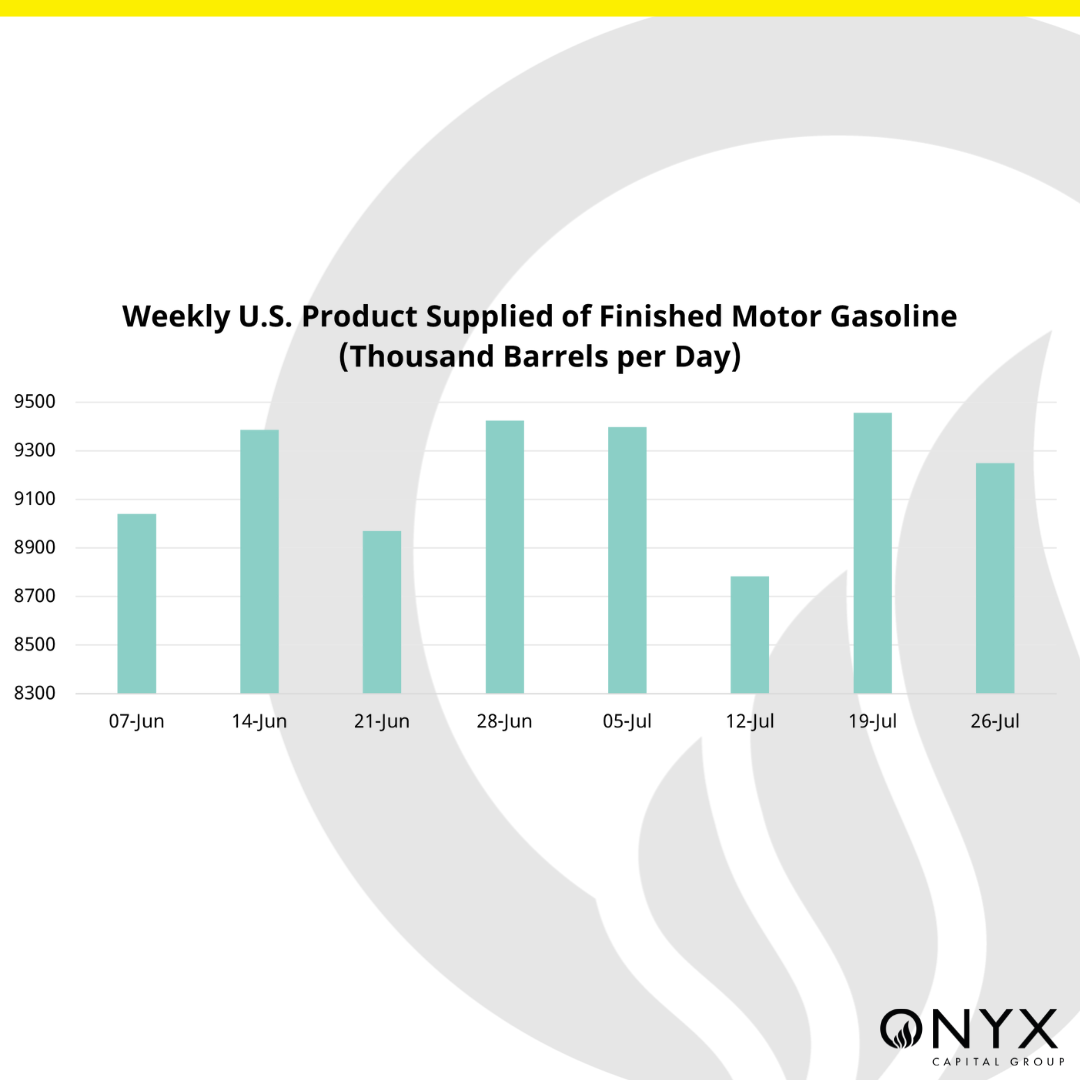

On 31 July, however, we witnessed two key drivers of sentiment: the Sep’24 Brent expiry and EIA stats for the week ending 26 July. The EIA reported a 3.436mb draw in US crude oil inventories, most of which was concentrated in PADD III (US Gulf Coast), which was consistent with the increase w/w increase in exports. Gasoline inventories also recorded a larger-than-expected draw in stocks, fuelling positive expectations for the US’ oil fundamentals. Interestingly though, product supplied of finished motor gasoline (a proxy for US gasoline demand) declined w/w declined. Also, while the EIA statistics were price constructive, they only provided temporary support to a market decidedly heading lower on gloomy macro data.

Activity survey data in China and the US was poor this week, with the Caixin and ISM Manufacturing PMI readings pointing to contraction. The rebalancing of US labour markets is raising concerns over the health of the US economy. Though US Fed Chair Powell green-lighted a policy rate cut for September, any positive surprise in inflation could derail the policy easing timeline. In other risk assets, US tech stocks and broader equity indices saw sell-offs amid these fears, while safe-haven assets like gold jumped up to a record of $2,500/oz. Finally, today’s data showed US non-farm payrolls rising by less than expected, alongside a rise in the US unemployment rate to 4.3% (prev: 4.1%). This data reinforces the expectation of a rate cut by the Fed in September.

Finally, geopolitical risk premia have crept back into oil prices following the assassinations by Israel of Hamas leader Ismail Haniyeh in Tehran and one of Hezbollah’s senior military commanders, Fuad Shukr, in Beirut. Threats of direct retaliation by Iran on Israel have added fuel to the fire. However, if any future kinetic actions remain within the realm of a ‘proportionate response’, with no threat to oil infrastructure, production or transport, then risk premia are likely to fade.