Lucky Number 85

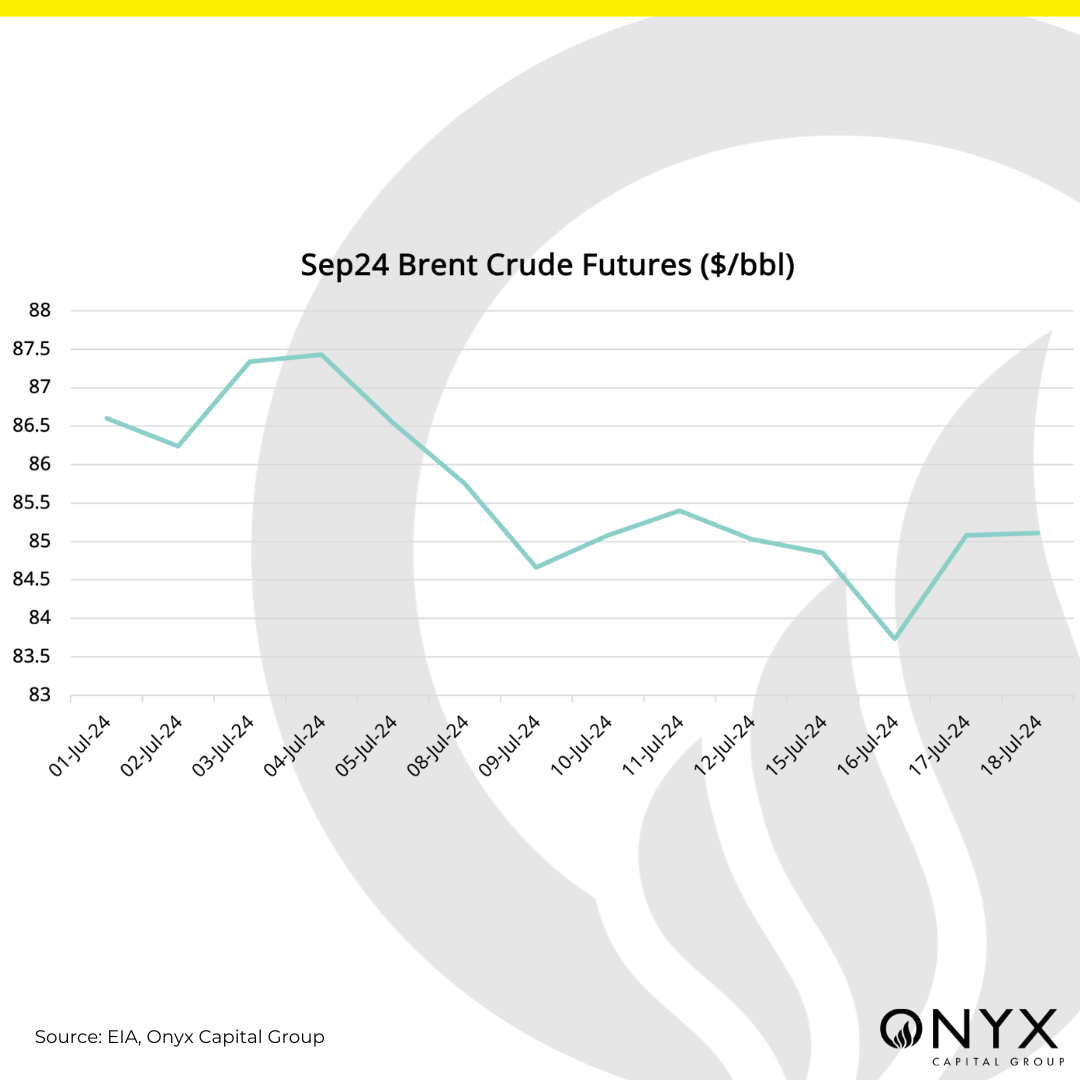

Price action in September Brent crude futures was resilient this week, oscillating around the $85/bbl handle. Brent came off to $83.50/bbl on 16 July before ascending above $85/bbl on 17 July, settling around that level in the subsequent days. This was within our $84-86/bbl forecast, indicating a relatively balanced market. The crude market has been driven by these factors this week:

- Strength in US crude

- Weakness in product cracks

- Expectations of sooner interest rate cuts

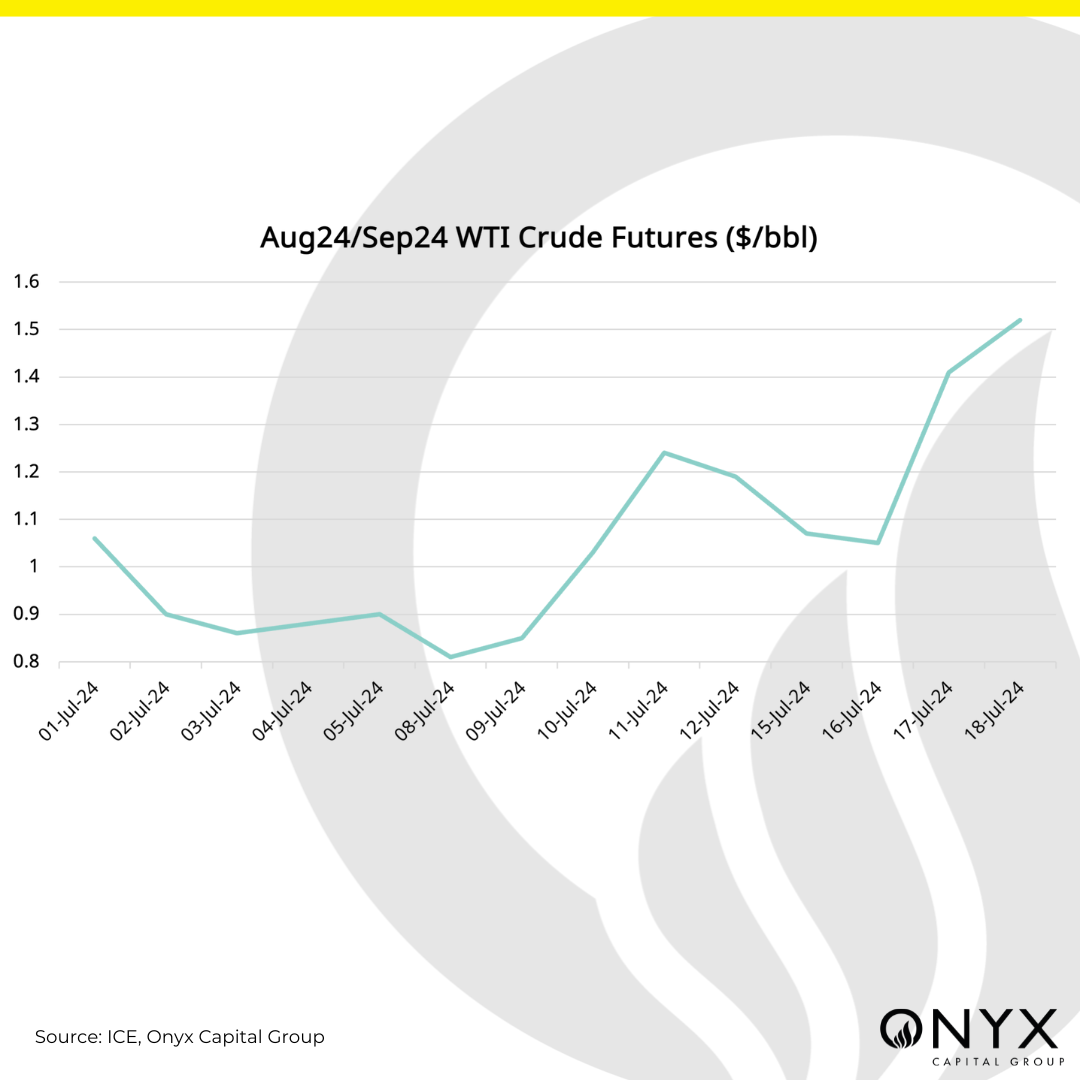

US crude (WTI) structure was well supported this week. Nearby futures prices are rising much faster than those for later delivery, with the Sep/Oct WTI futures spread gapping up from $1/bbl to $1.50/bbl on 17 July. The front-month September WTI futures contract expires on Monday 22 July. Hence, price action ahead of expiry suggests that a sudden scarcity in available domestic light sweet crude at the Cushing delivery hub may be at play. A similar trend occurred last September, where Nov’23/Dec’23 WTI futures reached $2.38/bbl highs. EIA stats were supportive, as US crude stocks saw a 4.87mb draw in the week ending 12 July. Weaker freight rates have opened the arbitrage between the Atlantic Basin and Asia, so physical traders seek to export US crude abroad. In line with this, the Brent/Dubai spread widened substantially, with refiners and banks on the buy-side according to Onyx counterparty type data, implying hedging interest.

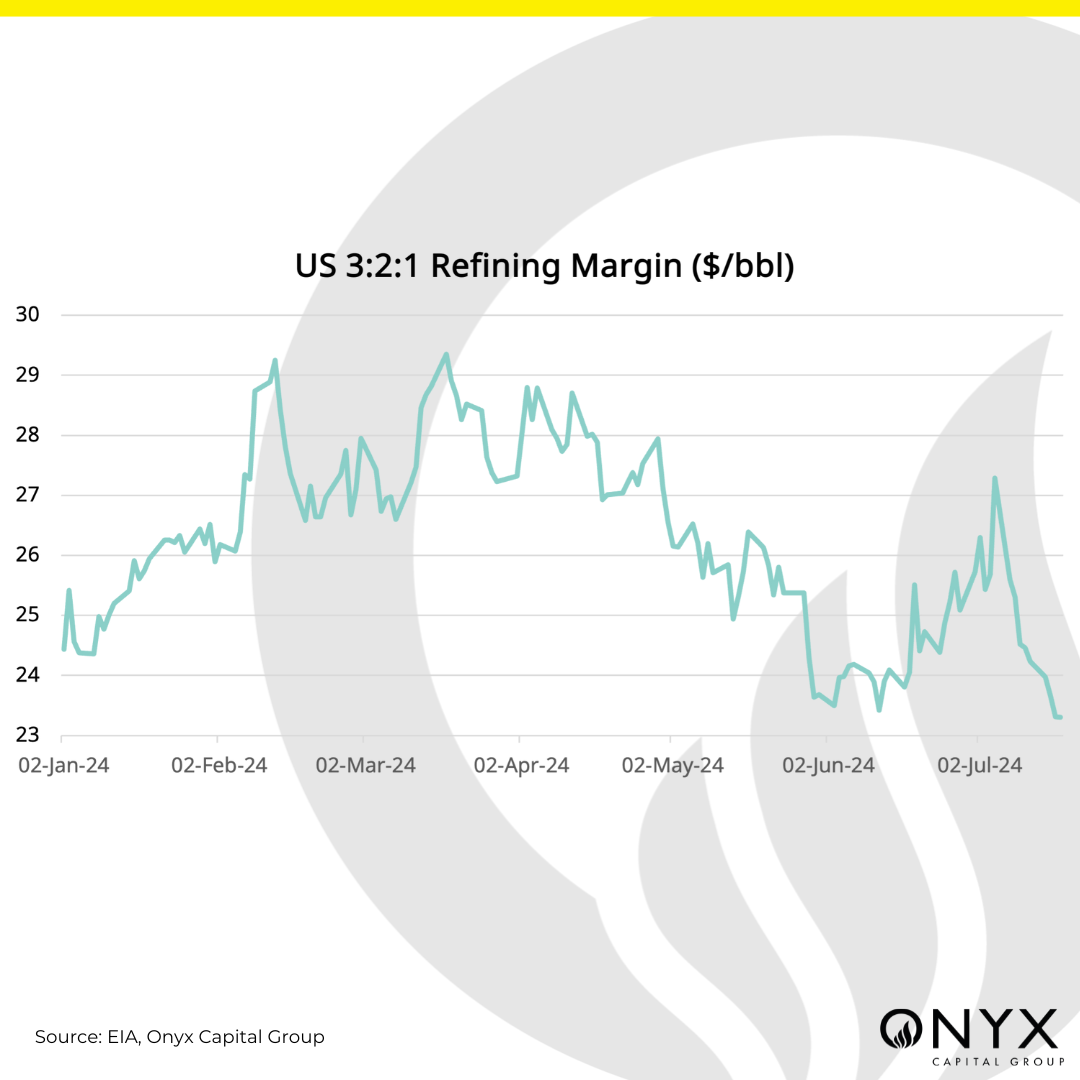

On the other hand, gasoline and gasoil cracks continued their downtrend, a bearish factor for crude demand. The product markets are adequately supplied amid lacklustre summer demand. The combination of weaker retail sales in the US, and the Gulf Coast producing ample supply on high refinery utilisation rates have pressured gasoline. Gasoil demand is sluggish, with front spreads in stable contango. Demand is expected to remain weak due to the onset of the monsoon season in South Asia. Moreover, EIA stats indicated larger-than-expected builds in gasoline and distillates, at 3.3mb and 3.4mb respectively. Encapsulating this is the struggling 3:2:1 US refining margin as it falls to 2021 levels rather than showing seasonal strength at this time of the year.

Crude prices benefitted from expectations of interest rates being cut sooner based on positive inflation readings. The annual inflation rate in the UK was at 2% in June 2024 – remaining at the target level – making a stronger case for interest rate cuts by the Bank of England. Meanwhile, the ECB left interest rates unchanged, but economists expect a cut in September as the bank downgraded its view of the eurozone’s economic prospects. US jobless claims jumped to 243,000 in the week ending 13 July. The softening labour market has bolstered expectations for a rate cut in September. Expectations of sooner rate cuts are bullish for crude oil prices as lower borrowing costs could boost oil demand.