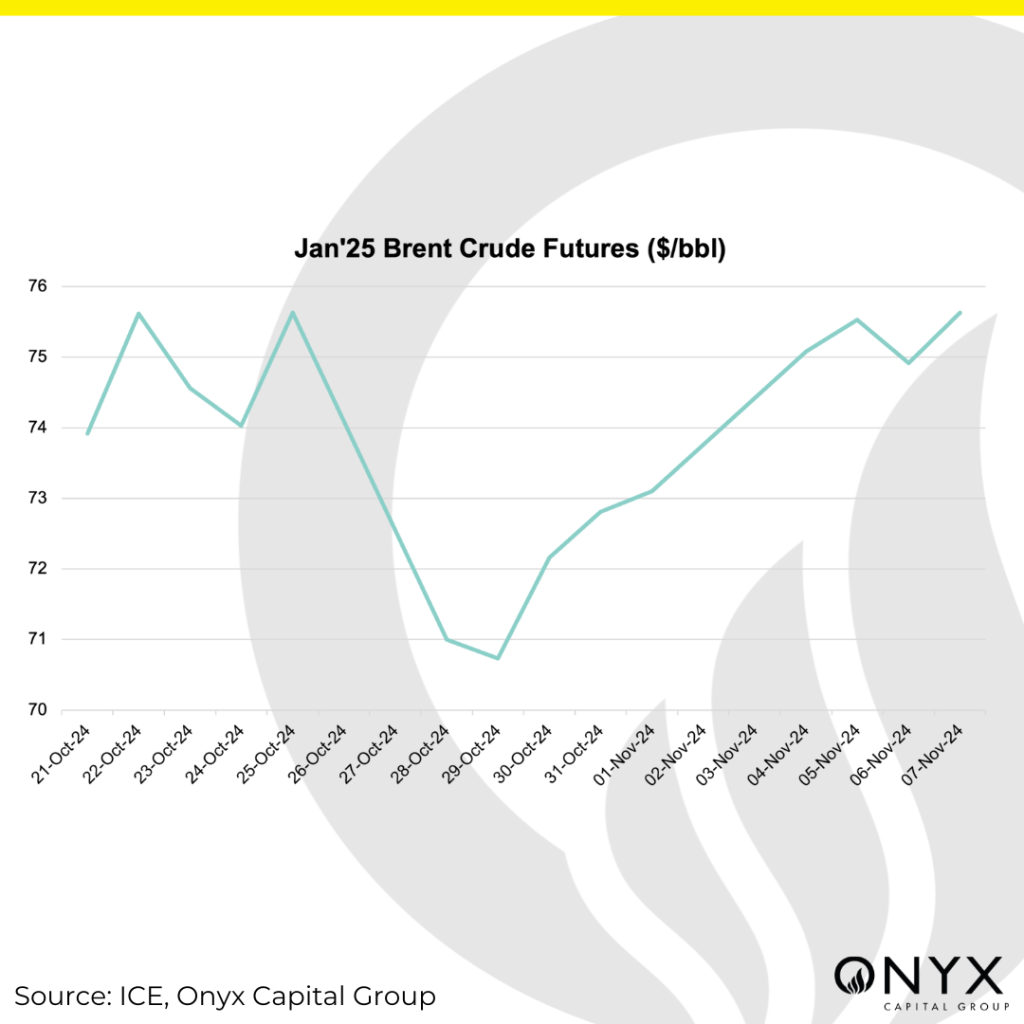

Brent crude futures saw a relatively rangebound week, with prices in the Jan’25 contract trading between $74 and $76/bbl. Oil’s reaction to the US election result was subdued, where the ‘Trump trade’ was focused on other risk assets, including equities, the US dollar, and Bitcoin. For now, prices are in equilibrium in the mid-70s, as the renewal of OPEC+ voluntary cuts is balanced against global macroeconomic headwinds. The key factors influencing oil prices this week include:

- Re-election of Donald Trump

- Hurricane Rafael

- Market Positioning

The reaction to Donald Trump’s re-election was initially bearish due to supply-side considerations but did not show significant movement this week. Jan’25 Brent crude fell during overnight trading on 6 Nov from $75.50/bbl to below $74/bbl. The FOMC’s decision to cut the policy rate by 25 bp came in line with expectations, but this did not stop the US dollar from rallying to its highest level since September 2022. In the meantime, traders mulled over the prospect of increased drilling and oil supply under a Trump administration. Markets are awaiting further clarity about the direction of US economic and foreign policy under Trump, which will have supply-side implications for oil. This will depend on the US’s sanctions policy against Iran and Venezuela and whether a lasting peace in the Middle East or Ukraine can be achieved, which could deflate the geopolitical risk that has buoyed crude prices in recent years.

In the longer term, the effect of trade tariffs will have ramifications on global economic growth and could induce a demand slowdown. Therefore, the impact of the incoming Trump administration on oil is complex and multifaceted.

Hurricane Rafael was in focus this week as its trajectory threatened crude oil production in the Gulf of Mexico, which provided some upside to price action. According to the Bureau of Safety and Environmental Enforcement, over 22% of crude oil production and 9% of natural gas output in the Gulf of Mexico was shut down in response to the storm. This amounted to 391kb/d of oil production and 181 million cubic feet of natural gas. However, as of Friday 8th November, supply disruption fears have receded as Hurricane Rafael is forecast to weaken and move away from Gulf Coast oilfields in the coming days.

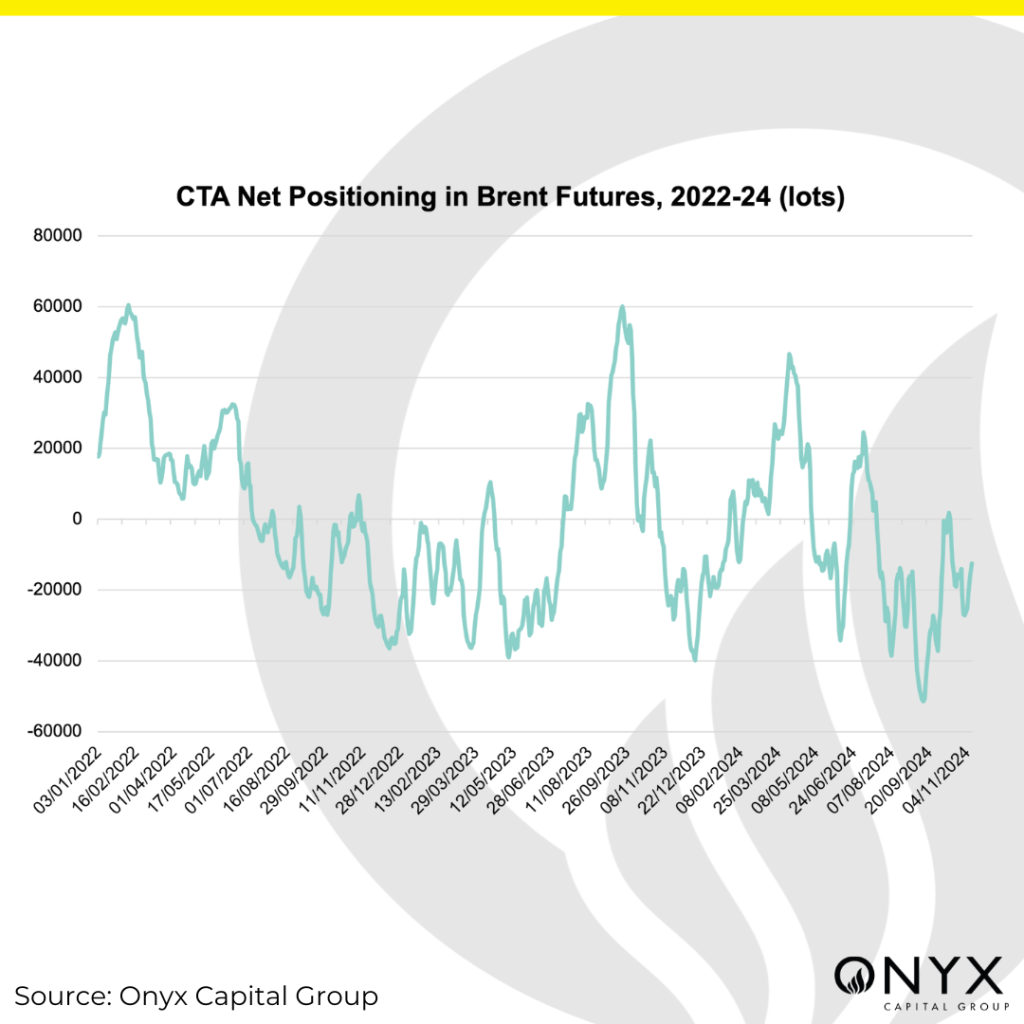

Finally, from a positioning perspective, the market is bearish on crude amid a weak fundamental backdrop. The managed by money long:short ratio in Brent futures has fallen for three consecutive weeks and is historically bearish at the 9th percentile for all weeks since 2013. Tonight’s ICE COT report will be updated for the week ending 5 Nov, revealing the state of the market’s positioning ahead of the US election results. Meanwhile, Onyx’s CTA model shows that while CTA positioning in Brent futures is on an uptrend, net positioning remains negative and is below the average level in the year-to-date. As market participants exhibit a bearish skew, short positions are becoming crowded, rendering price action vulnerable to a reversal in the event of a bullish catalyst.