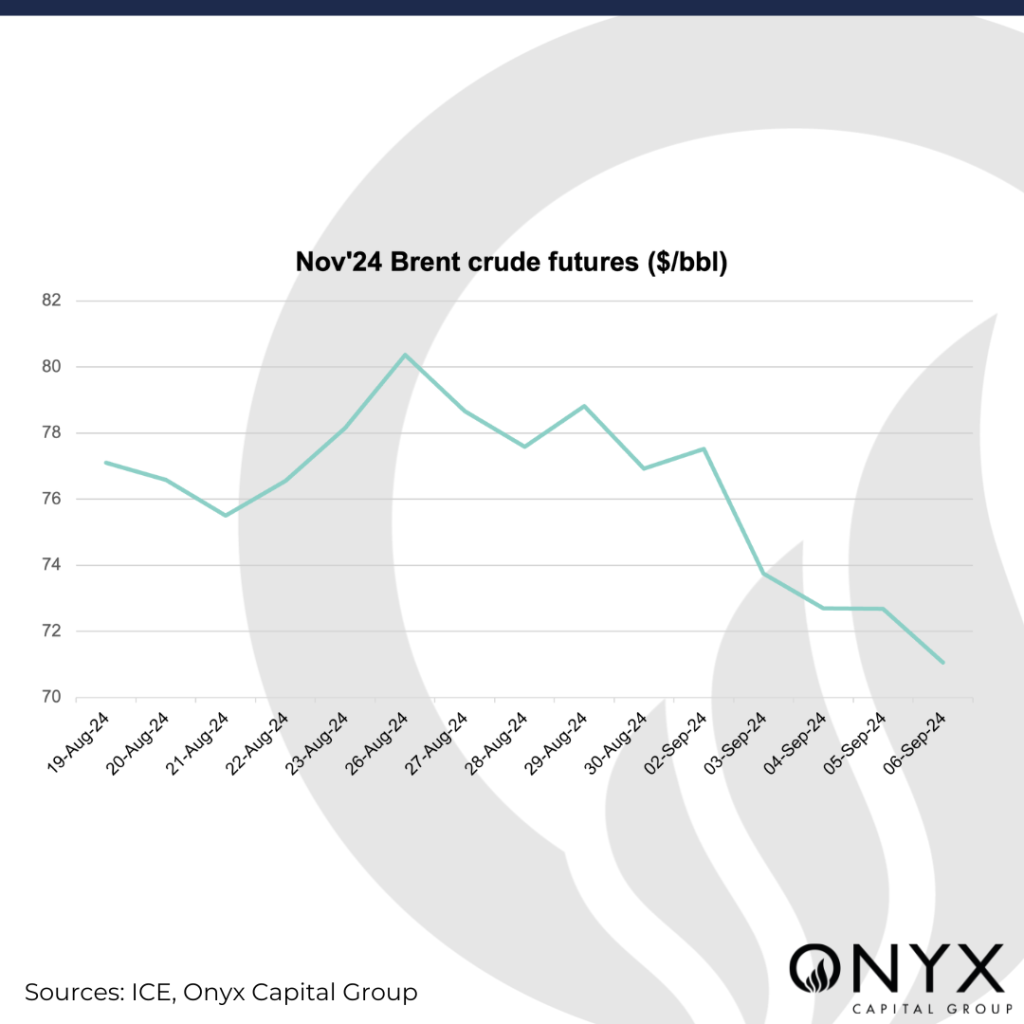

Brent crude futures saw a significant sell-off last week amid a weakening economic backdrop despite OPEC’s plans to delay its production hikes. The Nov’24 contract has stabilised at the $72/bbl level as of 09:00 BST (time of writing). While we expect no salvation for oil prices, we anticipate prices to remain above the $70/bbl level this coming week with a target of $71-74/bbl.

We will be closely keeping an eye on the following factors:

- Market Positioning

- Physical Market Weakness

- OPEC+ Compliance and Compensation

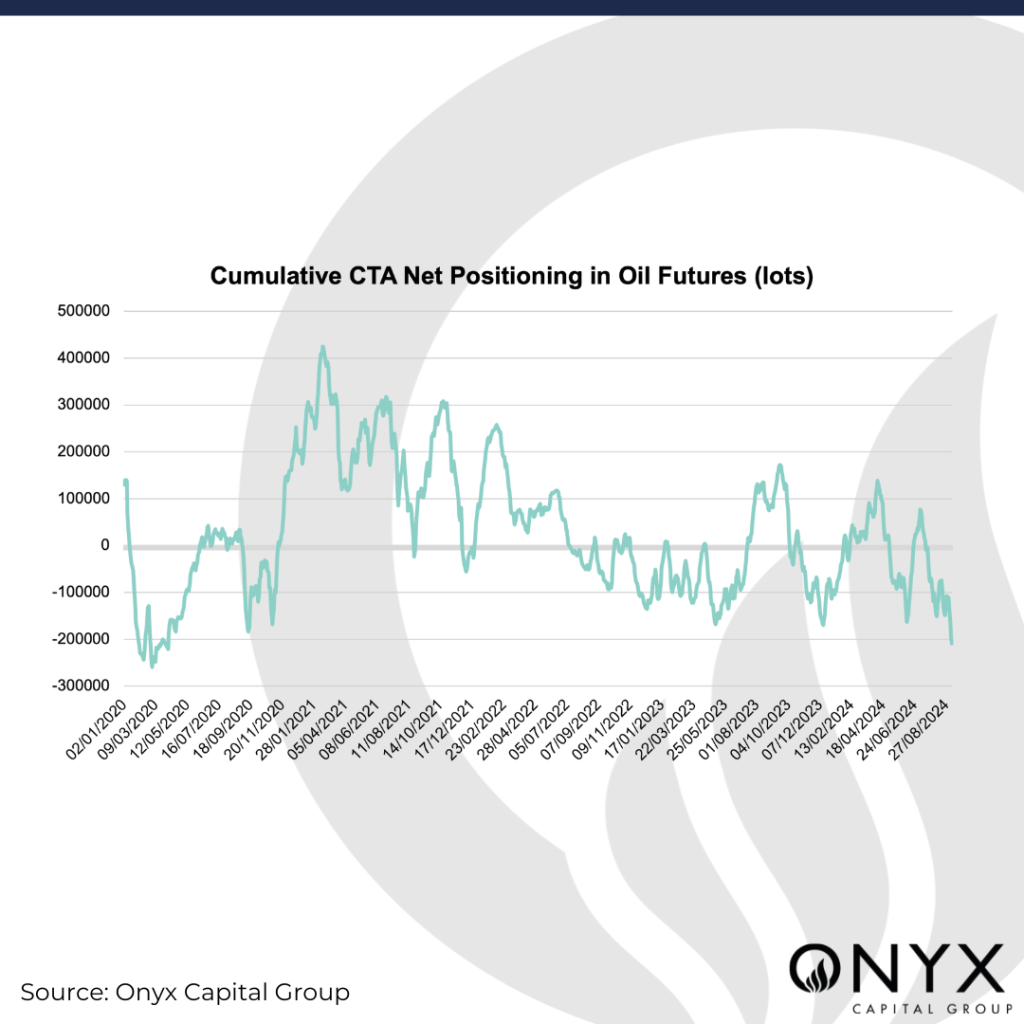

The latest CFTC COT data for the week ending 3 September indicates that money managers are historically short crude futures benchmarks. Combined positions in Brent and WTI futures reveal that net positioning is at the lowest level for over a decade. Bearish sentiment in WTI futures was the driver as its long:short ratio fell w/w from the 67th to the 21st percentile for all weeks since 2013. This comes as money managers redirect their attention from supply tightness concerns around the Cushing delivery point to questions of oil demand growth amid economic uncertainty. Meanwhile, Onyx’s CTA model reveals that net positioning in the oil futures benchmarks has fallen to the lowest level since March 2020, below -200k lots. This is a hugely bearish indication, as previous futures sell-offs in the past two years saw CTA positions bottoming out at around -160k lots. It has been speculated that some CTAs have increased their crisis alpha allocation, accelerating oil’s downside momentum. Nonetheless, with speculative crude shorts becoming crowded, they are vulnerable to reversal in the event of a bullish catalyst, such as geopolitical flare-ups or unplanned supply outages.

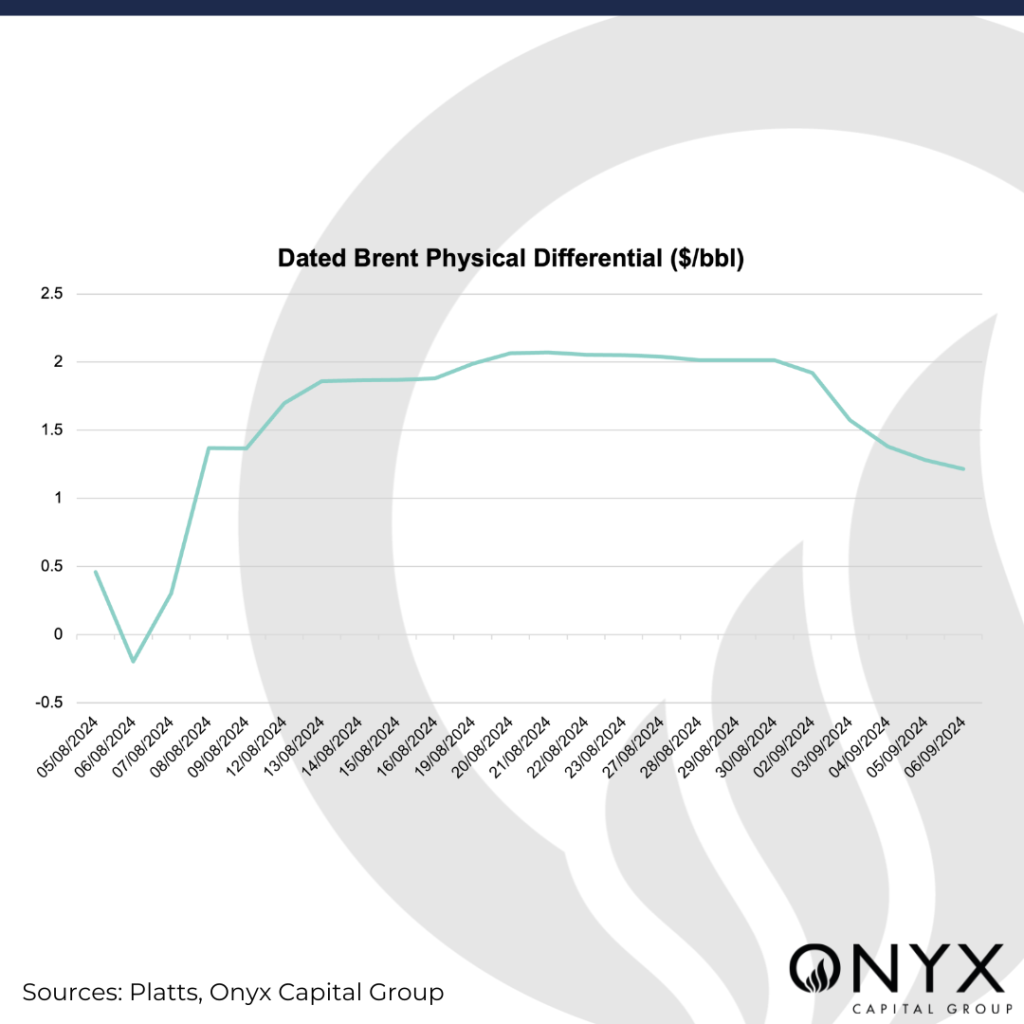

In tandem with the weakening futures market, the Dated Brent physical market has seen considerable downside pressure recently. Last week, multiple sellers emerged in the physical window as the supply situation improved, pressuring the physical differential down from $2.01/bbl to $1.21/bbl w/w. The tightness in the US market is easing, with WTI Midland setting the Dated Brent curve again. Moreover, economic uncertainty and weak refinery margins have weighed on sentiment, which may cause refiners to lower their utilisation levels. In addition, Dated-to-Frontline (DFLs) are in contango from the Jan’25 tenor, indicating expectations of an adequately supplied market. Although physical differentials have weathered previous sell-offs in Brent flat price, the weakening backwardation this time is a concerning bearish indicator, pointing to signs that the physical market is aligning with deteriorating crude fundamentals.

Going forward, compliance and compensation from Iraq, Kazakhstan, and Russia in their OPEC+ production targets will be critical for global balances, providing the breathing room for OPEC+ to add incremental barrels. Russia’s seaborne crude exports have been declining, while its Deputy Prime Minister Alexander Novak said that Russia’s oil output in August has been cut to the level required under the OPEC+ deal. The messaging from the producer group attempts to signal unity and collaboration, underscored by the OPEC Secretary General’s recent visits to Iraq and Kazakhstan. Kazakhstan has announced maintenance at the Kashagan oilfield, with cuts of 450kboe/d covering the promised compensation. Baghdad has cancelled a 1mb spot crude sale and will defer two more shipments, and reportedly has threatened to halt budget transfers to the Kurdistan Regional Government (KRG) unless production is reduced. However, the market’s reactions to these developments have been anything but bullish, and as the old adage goes, actions speak louder than words.