Show Me the Demand!

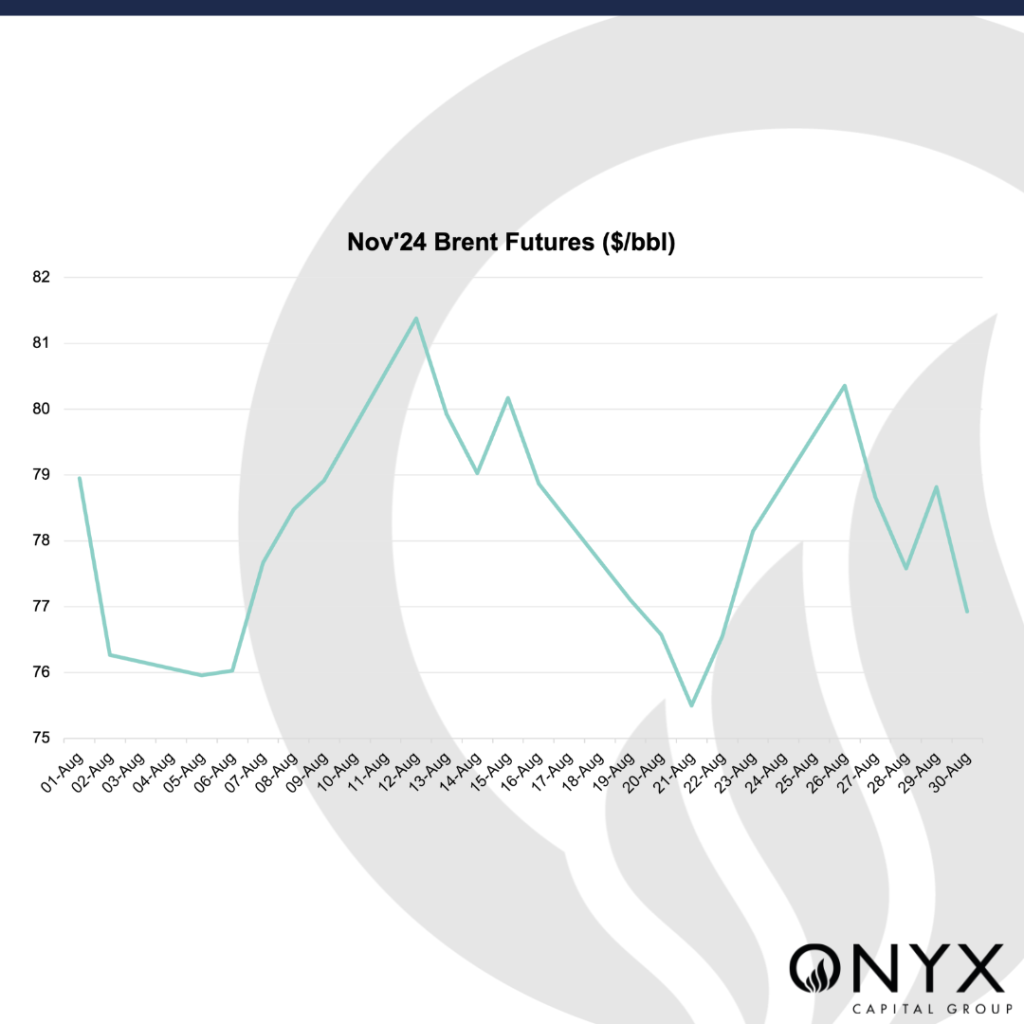

The Nov’24 Brent futures contract was trading at around $77.05/bbl at 09:00 BST (time of writing), and we expect it to end the week trading between $75-78/bbl. Amid the varying factors impacting the benchmark crude futures, we recommend keeping an eye out on the market’s reaction to three vital determinants this week:

- OPEC+ supply

- Weak China data

- Libyan oil fields begin production

At the end of last week, multiple sources from OPEC+ told Reuters that the producer group is set to proceed with its planned oil output increase following Q4’24, beginning with a boost of 180kb/d in October. This plan, which was decided upon at OPEC+’s 54th Joint Ministerial Monitoring Committee (JMMC) on 01 June, is part of a larger plan to gradually unwind its most recent layer of output cuts, equaling 2.2mb/d or 2% of the world’s daily oil demand, while keeping previous cuts in place until the end of 2025. This increase in supply generates a fundamental worry in markets: Is there any demand that could absorb this?

These concerns for demand are worsened by China, a vital oil consumer, reporting disappointing economic news. China’s official PMI index highlighted a slip to a six-month low of 49.1 in August, its fourth consecutive contraction. Another economic indicator, the Caixin/S&P Global manufacturing PMI, rose to 50.4 in August from contraction levels last month. However, considering that the Caixin PMI primarily covers smaller, export-oriented firms, this relatively upbeat PMI reading likely comes from an improvement in export orders – while China’s domestic consumption continues to languish.

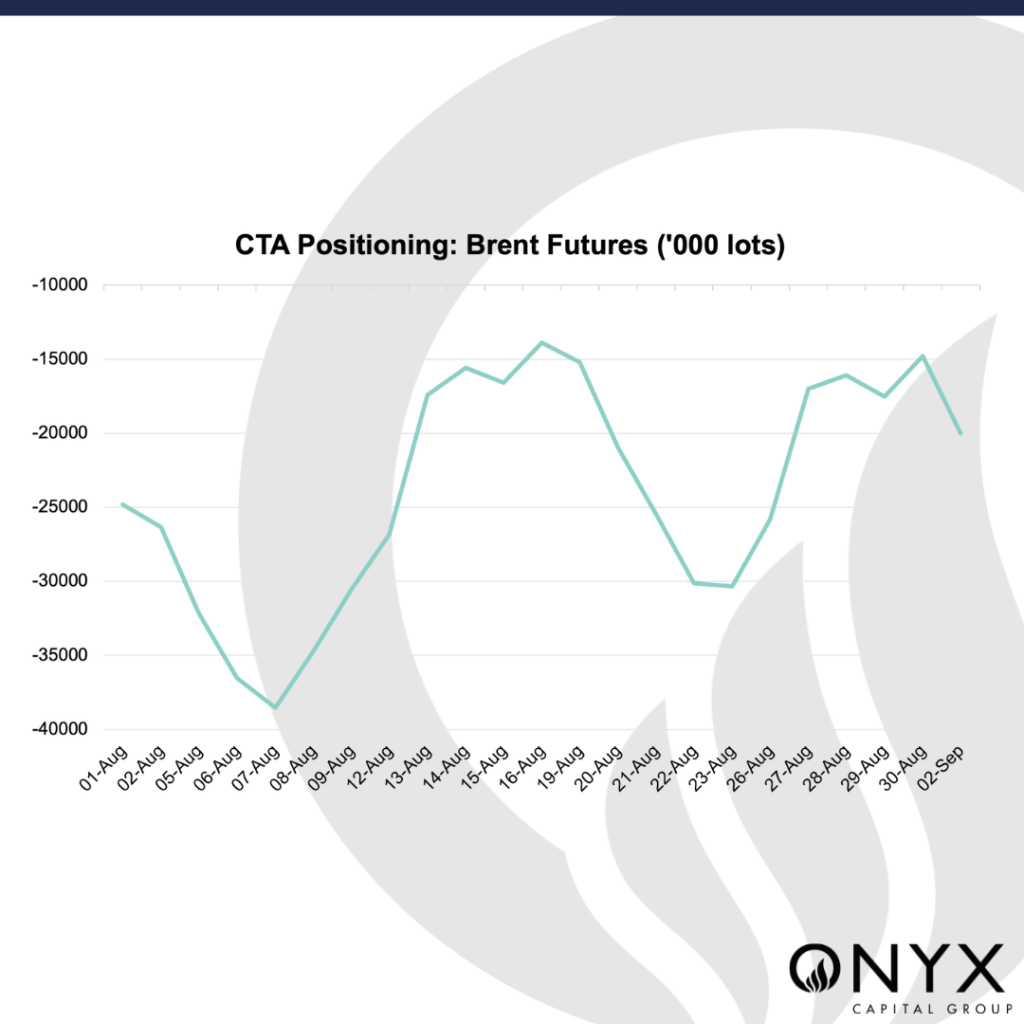

Finally, oil prices saw more relief last week amid supply outages in Libya over a conflict between rival political factions in a struggle to control the Central Bank of Libya. Alongside this news, Onyx’s CTA model revealed a 51% increase w/w in positions in Brent futures to -14.8k lots as of 30 Aug. However, Libya’s Sarir, Messla and Nafoura oilfields have now received instructions to resume production. While Libyan oil exports may remain disrupted presently, this news may soften the risk premia injected into Brent prices last week. Coupling this with the news on OPEC+ barrels, we may see further bearishness permeate into the market – evidenced by CTA positioning in Brent falling to -19k lots at the time of writing.