Lacking a spark

We expected Nov’24 Brent futures to end the week trading between $70/bbl and $75.00/bbl as we failed to see it breaking out of a rangebound market. Price action this week validated this view, with the contract trading at $71.85/bbl at the time of writing. As we recap this week in Brent, we highlight three points that were critical for sentiment and price action:

- COT positioning

- Economic news

- US-based fundamentals

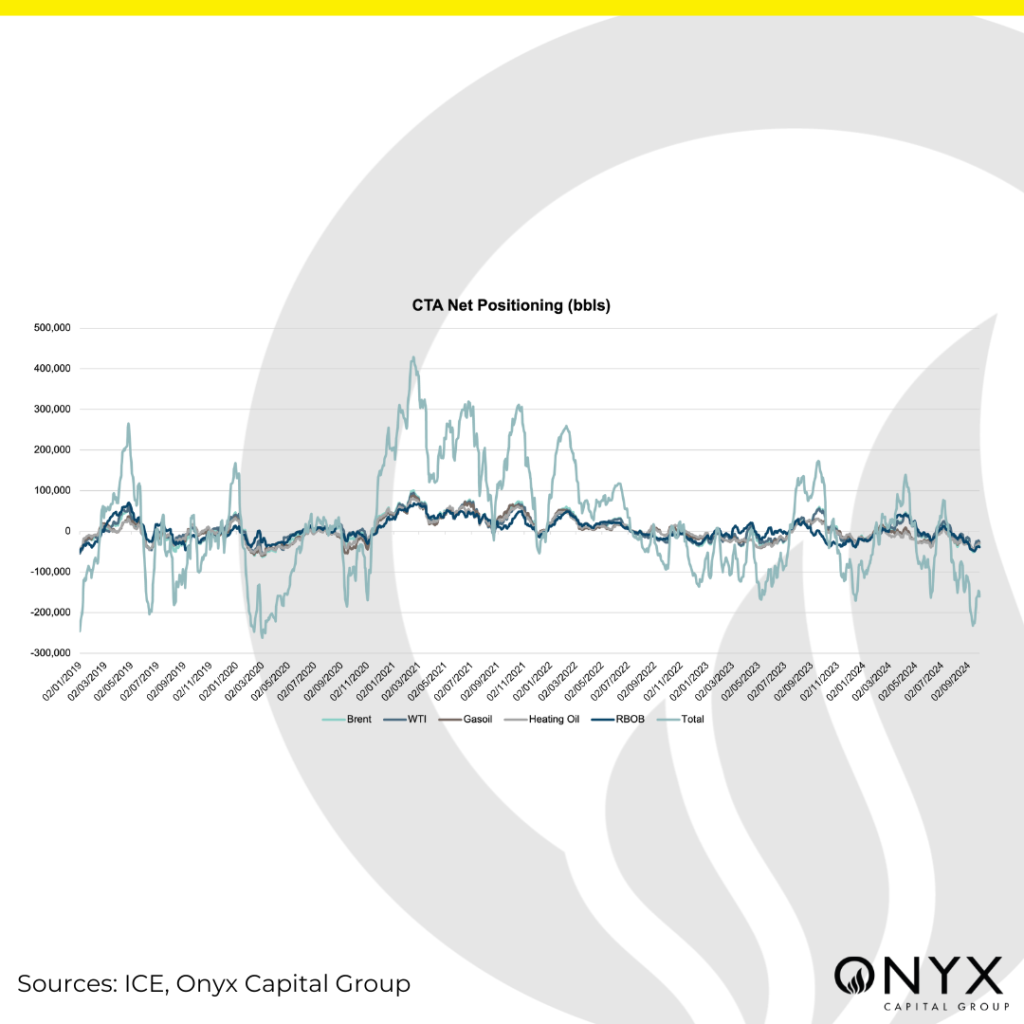

On Monday, we noted downside risks due to high short positions in Brent, with ICE COT data showing a risk-off stance and negative net positioning by funds. The Onyx CFTC predictor indicated continued risk-off attitudes from managed money and prod/merc players. Buy-side liquidity emerged with concerns over potential supply reductions from Hurricane Helene and the Israel-Hezbollah conflict, pushing Nov’24 above $75/bbl. However, this liquidity was sold off as Libyan factions agreed on new Central Bank appointments, and concerns grew over China’s substantial monetary easing, raising worries about the East’s economic situation. CTA net positioning lifted. A cycle low of -230kb was hit on 12 Sep, and net positioning has continued to increase, from -165kb on 20 Sep to -160kb on 17 Sep. This indicates a slight rebalancing in spec positions, although the market remains very short.

Economic news continued to be weak, and there was little to be bullish about. Chinese industrial profits fell sharply, which showed the harsh reality of China’s current financial situation versus the quasi-positivity of the stimulus headlines – which were quickly announced after the weak data. YTD industrial profits in China slowed to 0.5% growth over the same period last year. Monthly, August industrial profits were 17.8% lower than in the same month last year. We forecast that the economic news will have little impact on the market due to its positioning and the gloomy outlook by most players. This has proved fairly valid, although the vast capital injection from China into major banks is interesting to consider the impact of if it proves to be true.

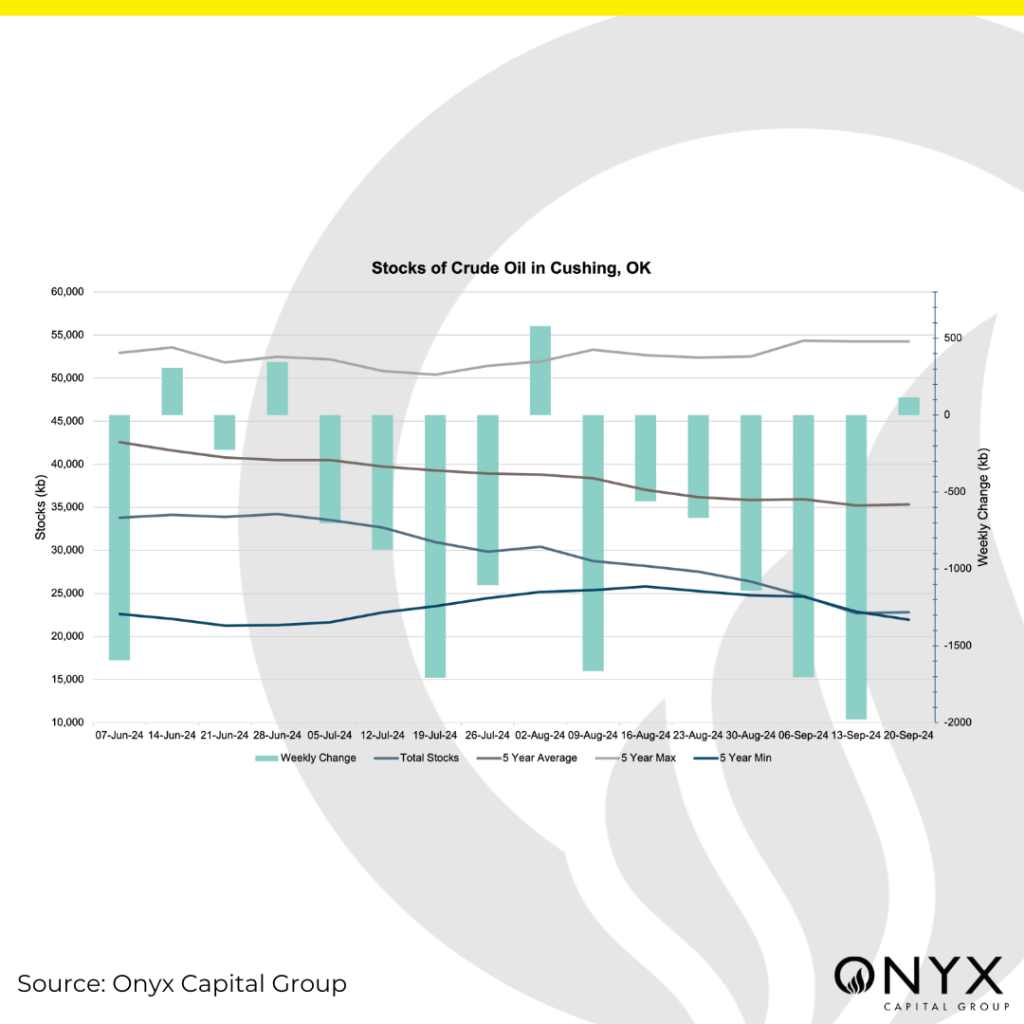

We foresaw that the US fundamentals would be of particular focus this week due to the low levels held in the delivery hub in Cushing, OK. These were at levels where operational constraints were becoming relevant, although they were within the historic range. EIA data for the week to 20 Sep showed a build in Cushing stocks of 116kb alongside exports and refinery utilisation falling more than expected, which softened this narrative.