Lacking a spark, continued rangebound prices in Brent.

We are looking for the front month Nov’24 contract to finish the week between $70-75/bbl as we fail to see any reason for Brent to break out of this rangebound regime. This call is predicated on three main drivers:

- COT positioning

- Economic news

- US-based fundamentals

ICE COT data for the week to 17 Sep showed a risk-off attitude prevailing in Brent Futures. Liquidation moved the market last week as both managed by money and prod/merc players removed long and short risk in Brent. This allowed the net positioning from funds and prod/merc players to increase and decrease, respectively. Net positioning for managed-by-money positions remains negative, showing funds’ extreme lack of optimism. Although there was a ticking up in CTA net positioning, this remains very low. Last week’s drivers include the impact of the 50bps interest rate cut from the Fed on Wednesday afternoon. The changes in positioning from this will be seen in the COT data released on Friday. This removed some uncertainty from the market, although the Fed have an optimistic view of GDP and unemployment forecasts. The Fed see unemployment peaking at just 4.4% in 2025 and GDP flat lining at 2%. This seems to have a high bar of consistent economic strength and may allow for greater volatility around employment data releases.

In economic news, the market has reacted bearishly to China’s efforts to boost the economy. Chinese youth unemployment hit 18.8% in August 2024 – the highest this year – up from 17.1% in July, reflecting ongoing economic challenges. There seem to be concerns about China missing the 5% growth target. The People’s Bank of China cut the 14-day reverse repurchase rate, signalling further monetary easing after similar July cuts. A rare upcoming press briefing by central bank governor Pan Gongsheng and top officials has fuelled speculation of increased stimulus measures. German manufacturing PMI fell for the fourth consecutive month to 4.03 and is now the lowest level seen in a year. US PCE released on Friday may have less impact than usual as the Fed’s next meeting is not until Nov 6-7, although inflation remains above the 2% aim. Therefore, we may not see any severe economic impetus this week.

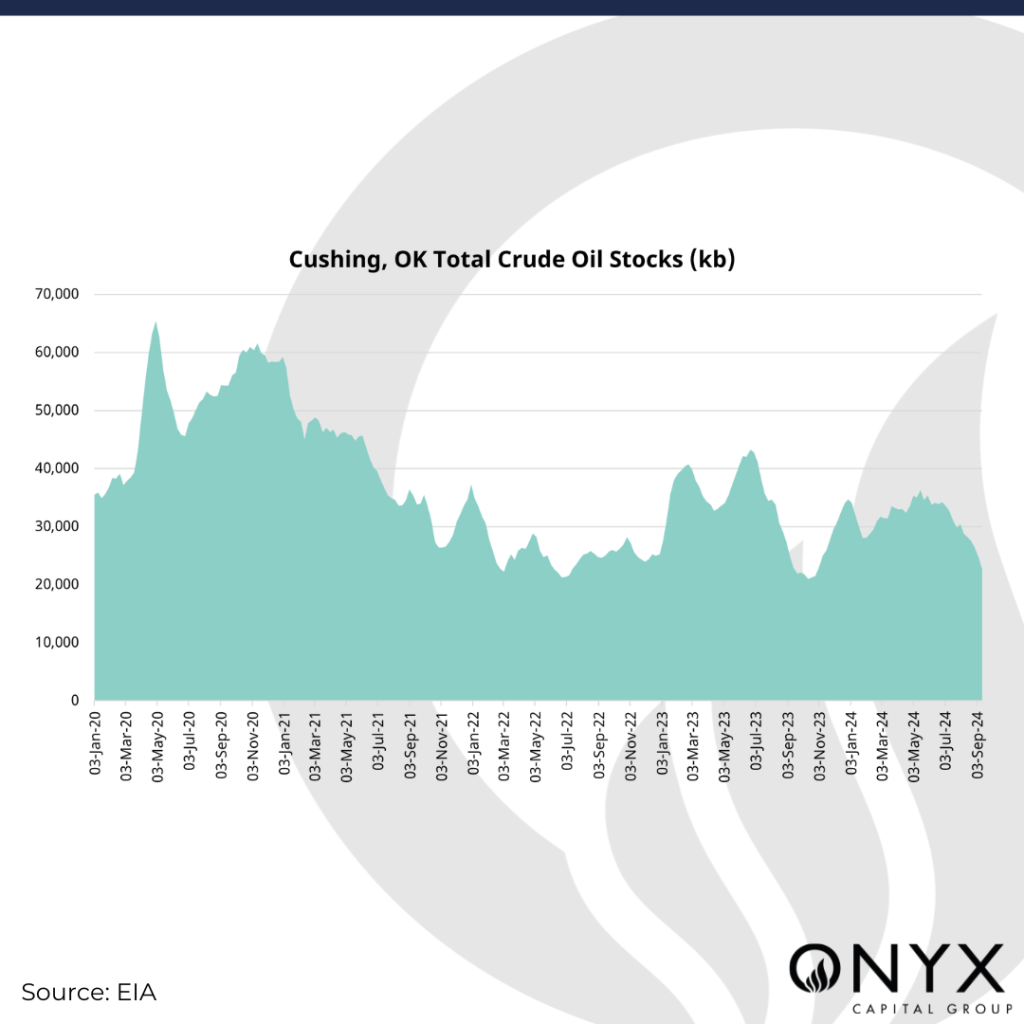

EIA stats released on 18 September showed further draws of crude oil stocks at the Cushing hub. Crude stocks in Cushing were less than 23mb. Cushing’s tank bottoms are estimated at circa 20 mb, and below 25 mb, there may be operational constraints. This has previously caused greater support for the WTI spreads, but we have not seen this to the degree expected. This could point to a sudden jump or underline the risk-off attitude in the market right now, as these lows are well-known and the market remains short, adding to the possibility of a more significant jump. Therefore, this week’s data will be of greater importance due to these low levels. Crude data, especially in the Gulf Coast, will be impacted by upcoming and previous weather events, so if these impact exports to a severe degree, keep an eye on weakening WTI spreads.