Geopolitical risk: down but not out

We see a firm Brent complex this week. We forecast Dec’24 Brent futures to end the week in the mid-70s, and we anticipate a ceiling of around $78, and $73/bbl acting as a floor. We expect oil prices to be buffeted by the following factors:

- Potential for geopolitical flare-up, and heightened volatility

- COT positioning and investor risk appetite, more shorts to cover

- US soft landing expectations means a less aggressive Fed

The drop in volatility following last week’s sell-off was especially noticeable, with perceptions of geopolitical risk receding somewhat and prices largely rangebound around $74.50/bbl between 16-18 Oct. However, this can easily change on a dime. A leak from the US military regarding Israel’s retaliatory plans vs Iran brought back some volatility into the game. If there has yet to be a direct retaliation from Israel on Iran, it does not mean the former has abandoned plans of striking military targets in its own time. A drone strike on Caesarea also points to this. Israel may feel vulnerable due to a permeable Iron Dome. Prime Minister Netanyahu said Iran’s strike was a “grave mistake”. We do not wish to underestimate the potential for geopolitical flare-ups pushing the oil price higher.

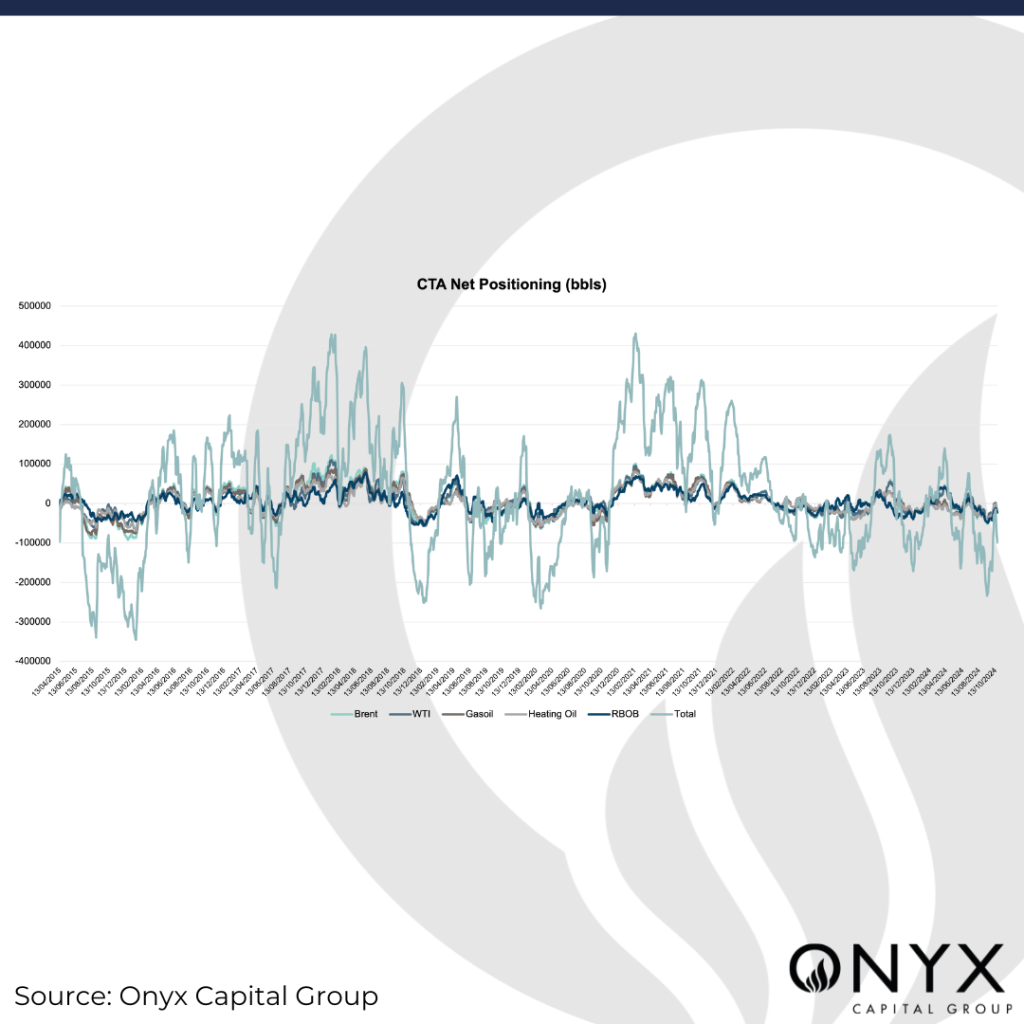

ICE COT data for the week to 15 Oct showed a modest retrenchment from funds. Money Managers saw their sell-side positions increase by 8.6% and long positions fall by 8.8%, showing an ongoing hesitancy to deploy risk. This is the first time in 5 weeks that we have seen this bearish regime from speculative players. The Onyx CTA data suggests that the market has become shorter following the 15 Oct cut-off for COT data. Our proprietary CTA model shows that participants are much shorter today than on 15 Oct when the official data cuts off. This subducts some bearish story from the market as it is so net short. This means that there are more short positions to be covered in the event of a geopolitical development that could also push the oil price higher from a flow perspective.

Without major releases from Europe and Asia, barring flash PMI estimates in Europe, the macroeconomic focus swings back to the US. The positive data released last week in the US has set up some more optimism for a soft landing in the economy. The nonfarm payroll at the beginning of the month showed unemployment dropping to 4.05%, and the latest initial jobless claims declining month on month. We have also seen US retail sales improve by 0.4% and 1.7% y/y, with strong wage gains and back-to-school spending. Data released this week is likely to be muddied by the impact of hurricanes and an ongoing strike at Boeing. So, the market will probably focus on Fed speeches before the blackout period starts on 26 October – which are likely to focus on cutting interest rates at a gradual pace rather than out-sized reductions of 50 bp, which may prove disappointing to risk assets.