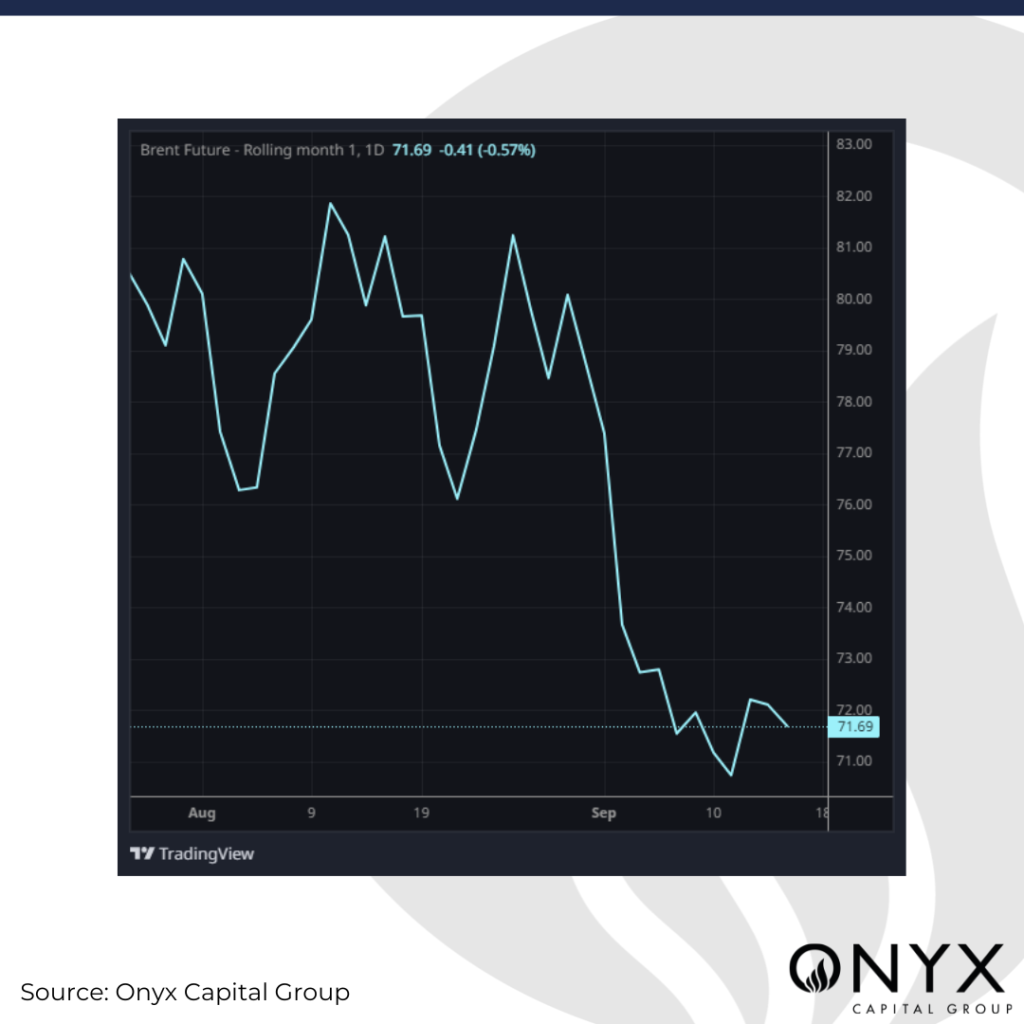

Is $70/bbl the new $80/bbl?

The Nov ’24 Brent futures witnessed a tumultuous last week, briefly falling below $70/bbl for the first time in three years before finding support here. While the benchmark crude oil futures contract remains above this crucial support level, we expect Brent prices to reset and oscillate around a new lower equilibrium price for now, remaining rangebound at the end of this week between $71-74/bbl.

We further recommend keeping an eye out on the following drivers this week:

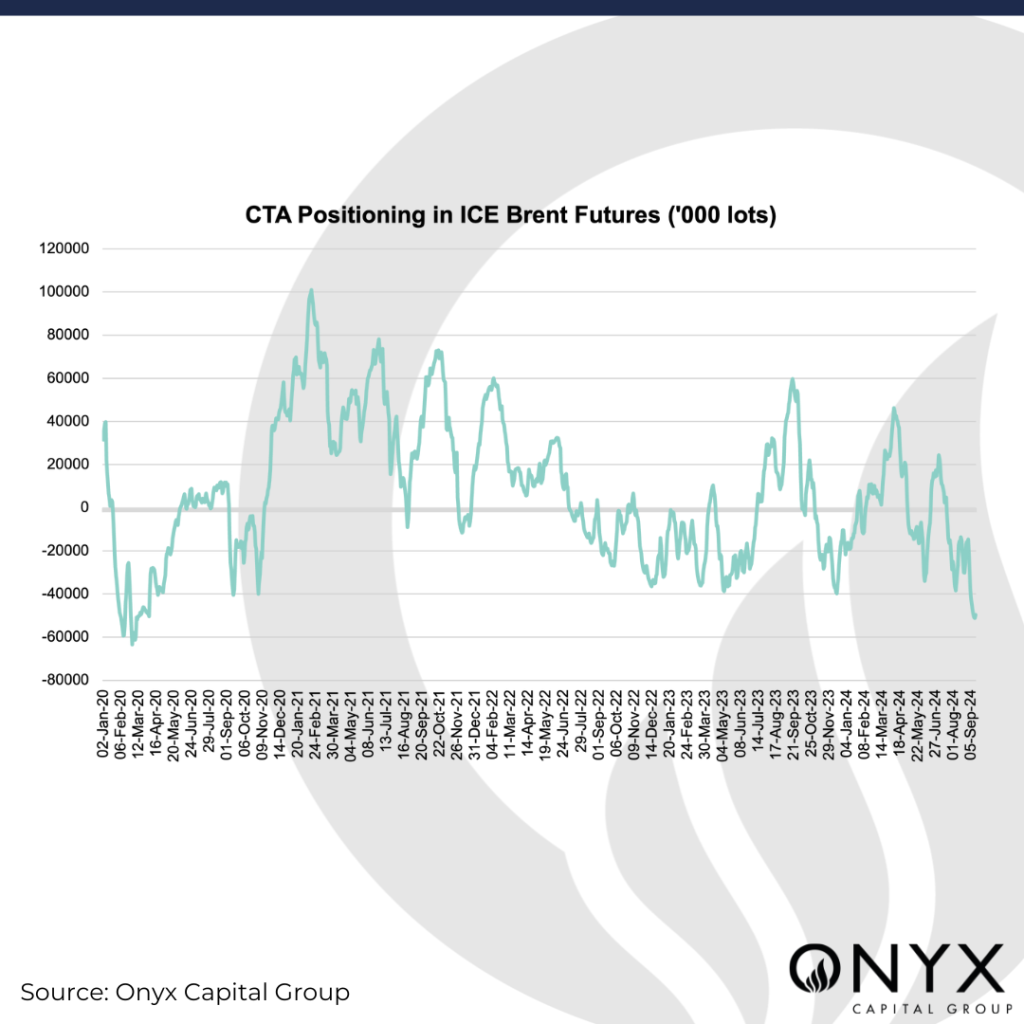

- CTA positioning, following Brent’s COT net positioning dipping below 0

- Loosening US Supply post-Hurricane Francine

- US Fed FOMC Meeting amid a cooling labour market

COT data for the ICE Brent futures contract in the week ending 10 September highlighted that speculative players removed an additional 35mb from their long positions while adding over 23.6mb to their shorts. This shift in positioning reduced the cumulative net length (longs minus shorts) in the benchmark futures complex to -33.7mb, taking money-managed positioning net short for the first time in history. While this positioning accentuates the bearish sentiment in oil, we may be seeing overcrowding short positioning in Brent futures now and expect some respite for the futures complex in the near term as some short-positioned players exit to take profit. Additionally, CTA positioning remains extremely short, with Onyx’s CTA model sitting at -51k lots on 13 September – putting CTAs at a prime spot to retrace upwards from this extreme positioning. A final point here in favour of Brent is that COT data for the week ending 10 September also saw producers/merchants flip to adding substantial long risk in the futures for the first time in six weeks, adding 44mb to length. This change likely emerged alongside a rise in activity by natural crude oil buyers, like refiners, at this low level.

However, positive price movements may be capped by US crude oil producers returning to normalcy following disruptions in US Gulf of Mexico oil and gas, which had kept prices supported early last week. We now see these supply disruptions easing, with refineries in Louisiana now resuming operations and the US Coast Guard reporting that the Louisiana Offshore Oil Port (LOOP) was back online without restrictions last Friday. Still, negative price movements may also find a floor, with the US Bureau of Safety and Environmental Enforcement estimating that 20% of crude oil production and 28% of natural gas output in the US Gulf of Mexico remains offline as of 15 September. However, if these supplies swiftly come online this week, it would contribute to further bearishness.

Finally, we expect volatility this week as markets await 18 September’s US Fed FOMC meeting. Despite pricing a 25 bp cut last Thursday, the market is now pricing in a cut of 39 bp, with Fed fund futures now pricing in a 59% chance of a 50 bp cut in Wednesday’s meeting. This change comes alongside a shift in US consumer sentiment. While overall consumer sentiment sat at 69 in Sep ’24, the highest observed level since May ’24 (Aug ’24: 67.9), sentiment regarding the labour market softened. The share of consumers expecting the unemployment rate to increase over the next year rose to a 16-month high of 39% in Sep ’24 (Aug ’24: 37%). A cooling labour market may induce the Fed to opt for the more aggressive 50 bp cut on Wednesday. It will be interesting to see how the market would react to such a cut: On the one hand, it may inject support for risk assets such as oil. However, it may also cement fears of a US recession, which, alongside China’s beleaguered economy, may pressure the outlook for oil demand.