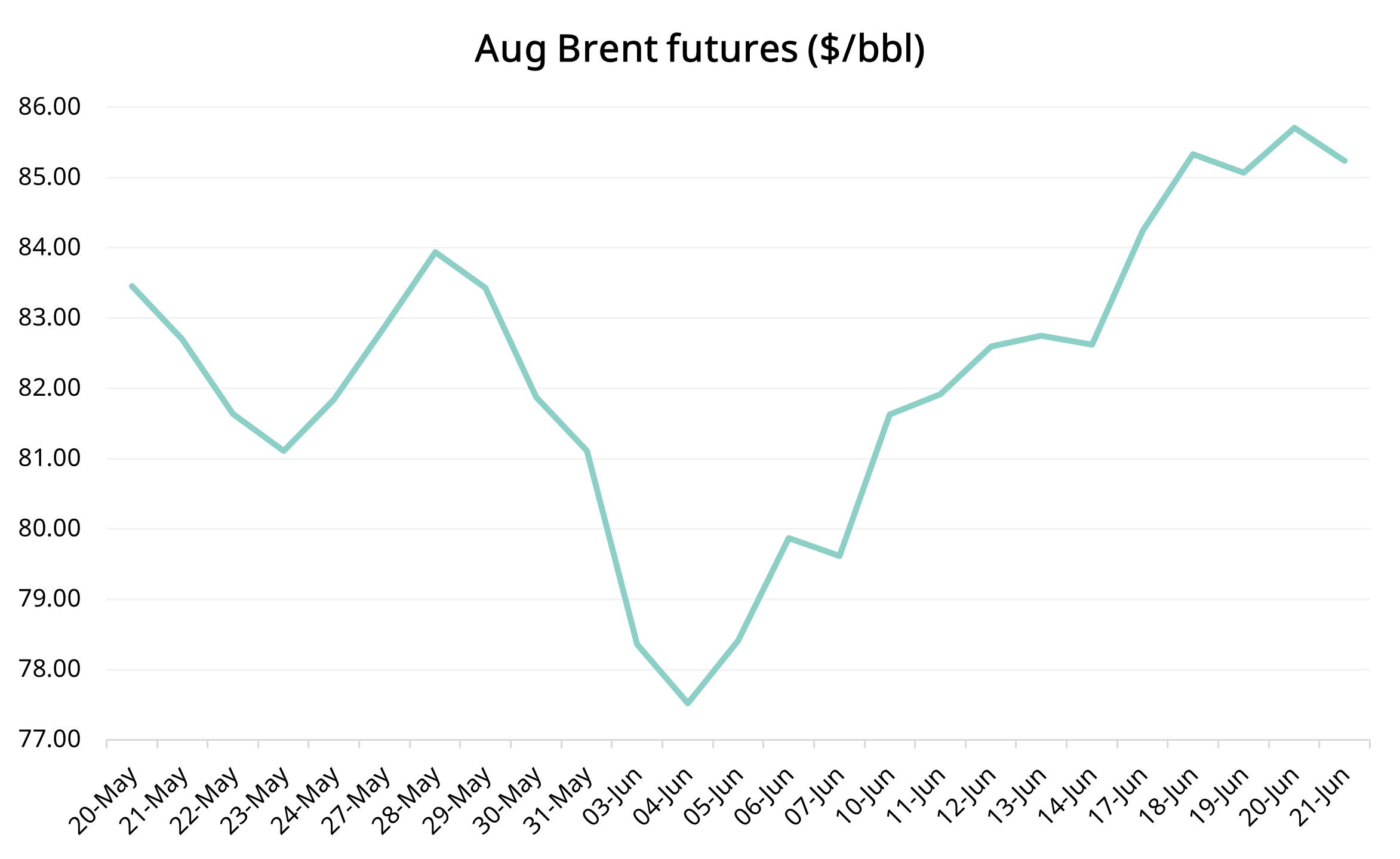

TARGET PRICE: $83-85/bbl

Too close to the sun?

The prompt Brent futures flat price contract recorded great strength last week. The contract began the week at $84.25/bbl and rallied past the $86/bbl handle on 21 June – where it met resistance. We now see the contract hovering around $85.30/bbl at 08:30 BST (time of writing), although we anticipate short-term bearishness to take the benchmark crude futures to $83-85/bbl by Friday. This expectation emerges out of three key factors:

- The US dollar’s strength

- Possible profit taking from in-the-money longs

- US fundamentals

Oil sentiment has improved recently relative to the past month. The difference between Dated Brent and Brent swaps for July rallied from an intraday high of -3c/bbl on 04 June to 85c/bbl on 19 June. This strength indicates the entry of the long-awaited “summer demand” this year and is expected to keep oil prices supported in the medium term. In the short term, however, we expect a slight correction. The primary reason for this belief is the US dollar’s recent strength.

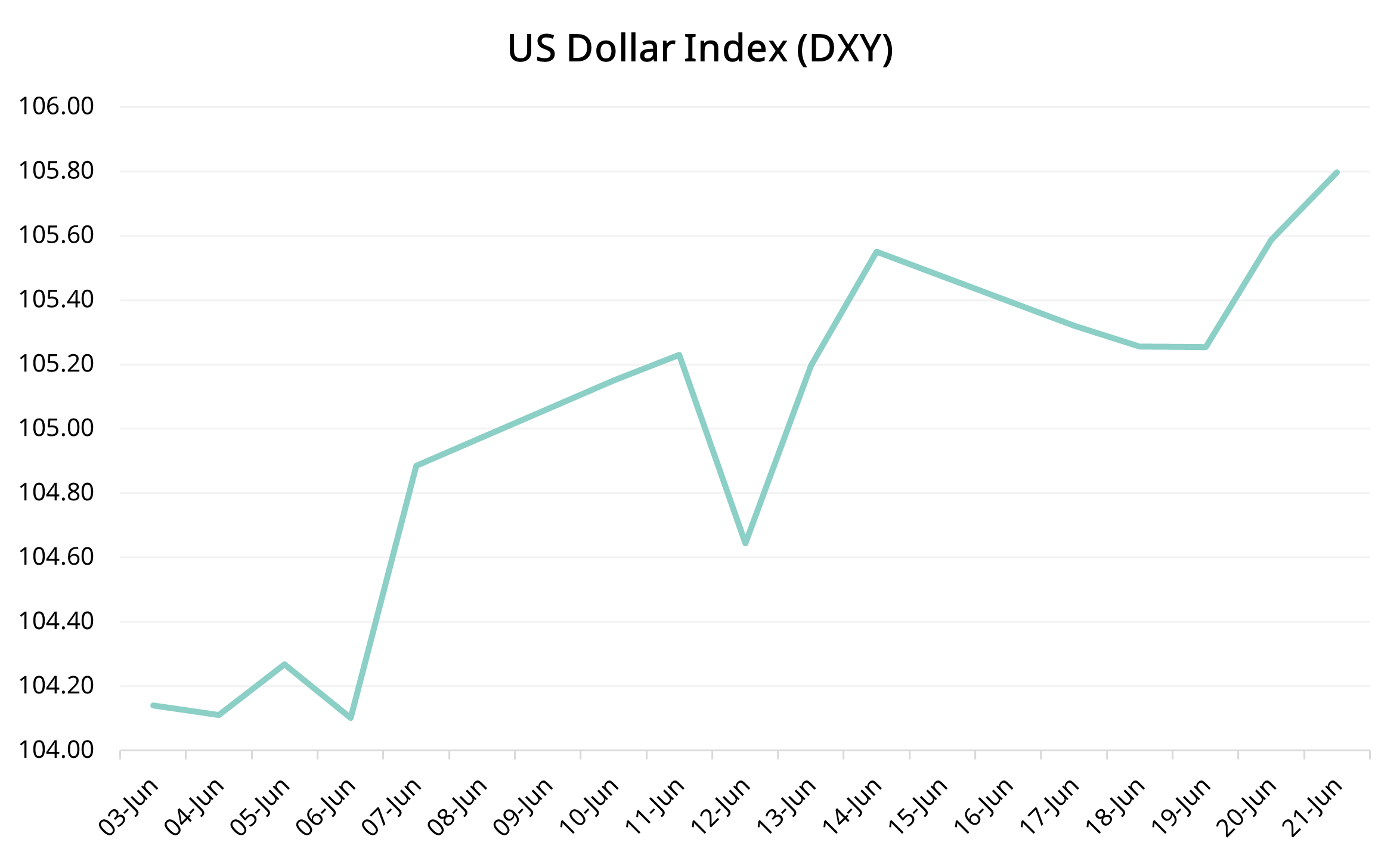

US activity surged to 54.6 last Friday (prev: 54.5), the highest reading since April 2022 – as per S&P Global’s flash US Composite PMI Output Index. In addition, both the services and manufacturing sectors were stated to have contributed to this gain. This claim of robustness in the US economy raised concerns about a further postponement of interest rate cuts and lifted the US dollar index (DXY) to 105.88 on 23 June, its highest level in two months. Other currencies weakened relative to the USD, with the yen coming off to 159.94 per dollar in early trade on Monday – its lowest since 29 April. A stronger dollar, relative to other currencies, makes the dollar-denominated oil more expensive for players holding other currencies.

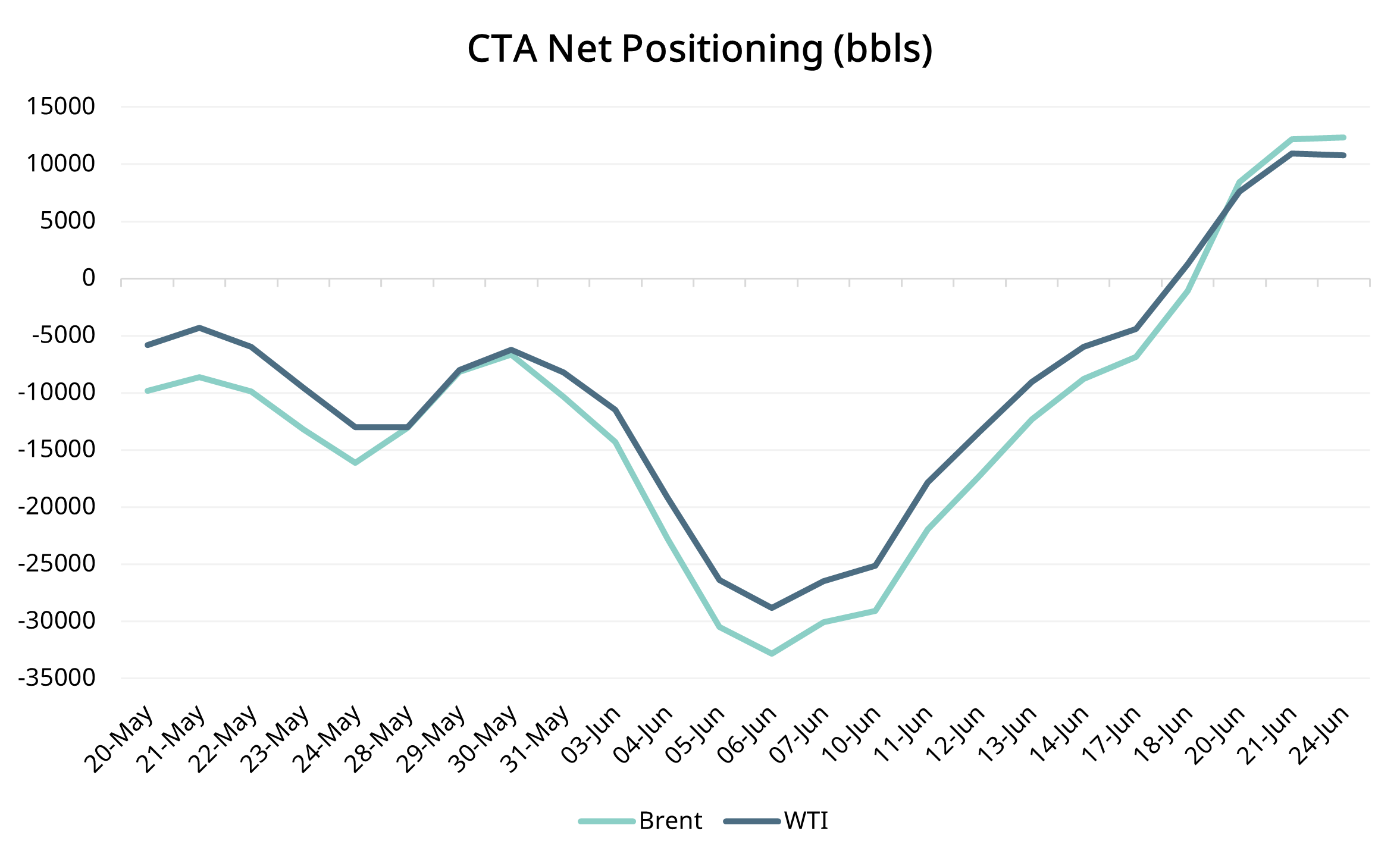

Our second factor is the expectation that in-the-money longs could now take profit. Both the Onyx CTA positions model and the ICE COT report showcase a rebound of total managed-by-money net length over the past week, indicating new length alongside possible short covering behind last week’s strength. While we have yet to hit an extreme end in net length as per the CTA model, highlighting further room for bullish positioning over time, we anticipate a slight dip in length over profit-taking, contributing to short-term weakness.

Finally, we recommend keeping an eye out for fundamentals in the US, particularly US exports. With the rise in Dated Brent, we expect to see more cargoes entering Europe from the US. This influx in supply may elicit a bearish response from players. However, we recommend monitoring the EIA’s data on US oil inventories this week. If we see a significant draw in crude oil stocks, we may instead see prices rally further.

Sentiment Wildcard

The two oldest candidates ever to run for the US presidency, President Joe Biden and former President Donald Trump, will meet this Thursday for a televised debate. Unlike previous US presidential debates, this event may also test both candidates’ cognitive abilities in addition to their policies, making its outcome all the more uncertain and a definitive wildcard for sentiment in the oil markets by the end of the week.