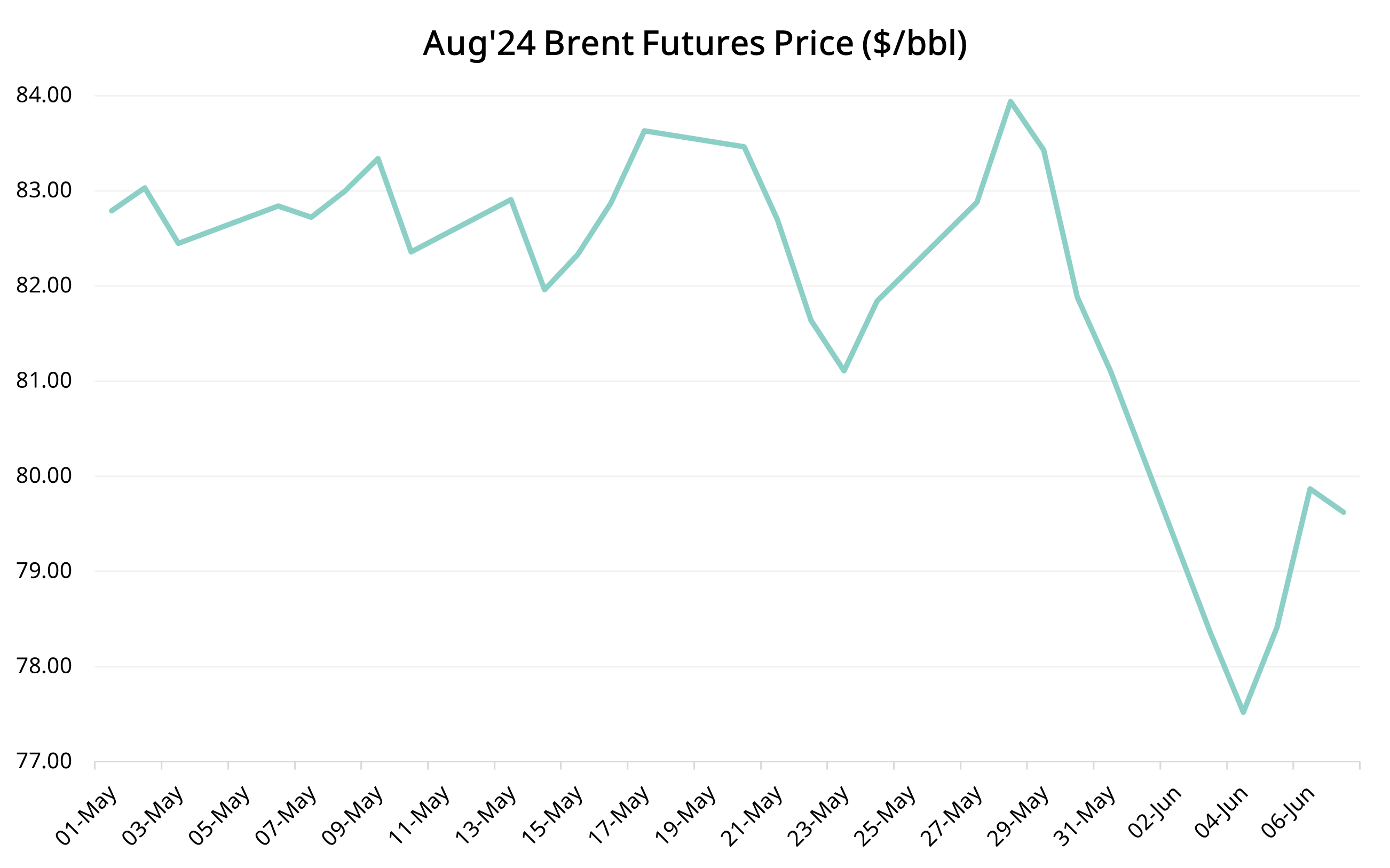

TARGET PRICE: $78-80/bbl

We expect Brent to trade on either side of $80/bbl this week, with a slight bearish bias. We are looking for the front month August contract to finish the week between $78-80/bbl. This call is predicated on three main drivers:

- USD strength

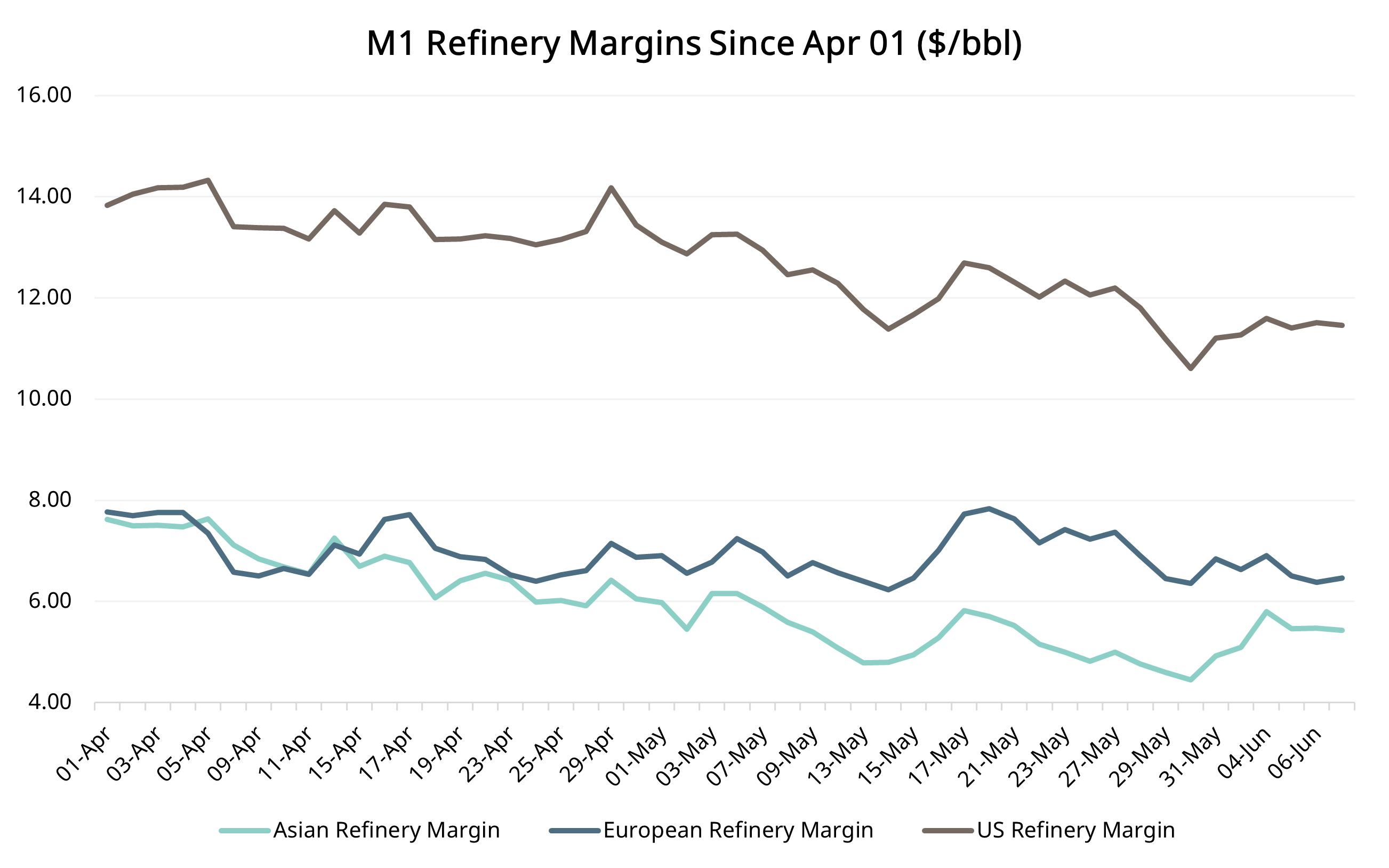

- Weakness in refinery margins

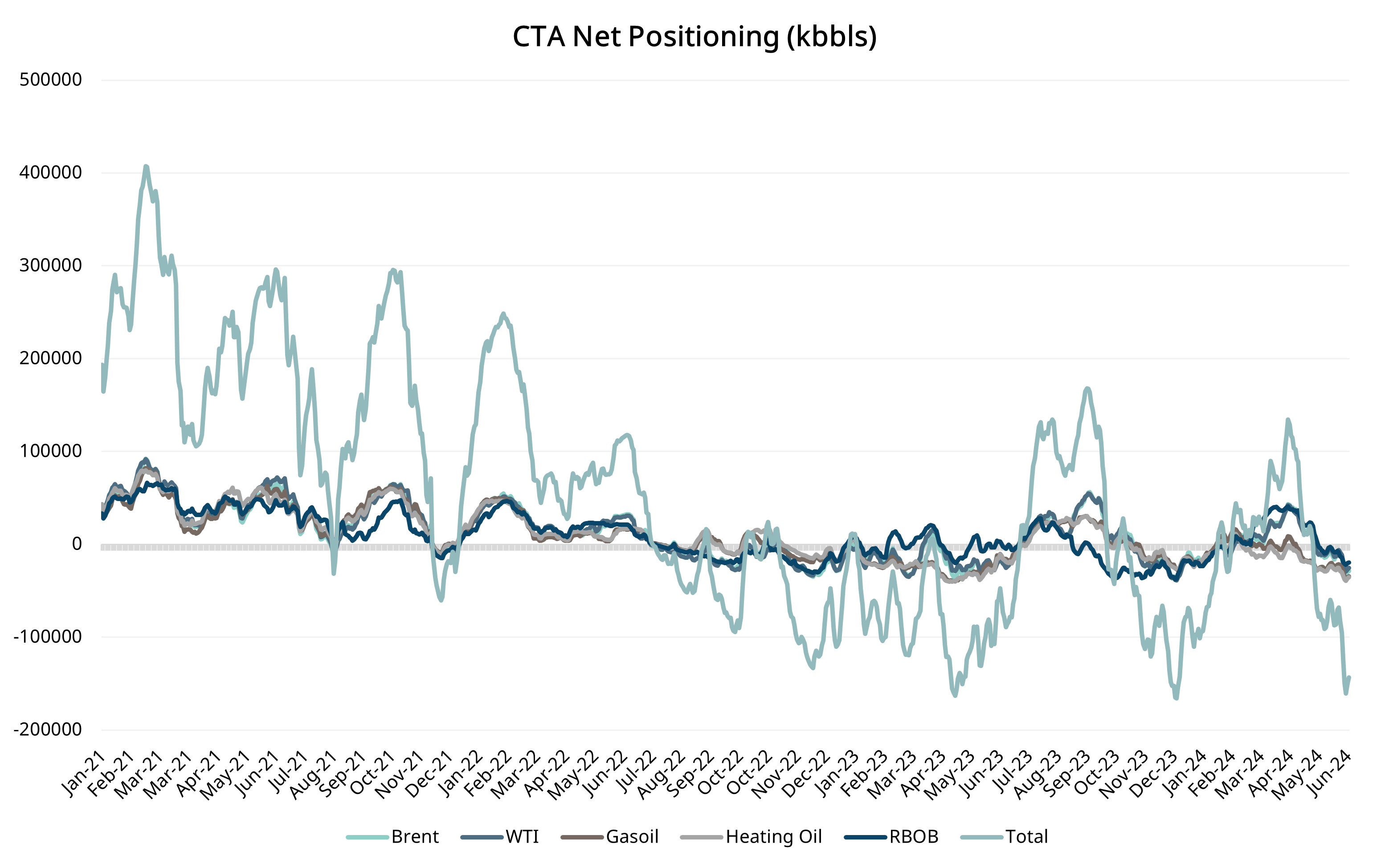

- Very short market positioning, which can easily unwind

In our view, there fails to be a compelling, strong, bullish story for Brent to move sustainably higher in the very short term. First, on the macroeconomic front, an unexpected positive development in US labour markets raised speculation that the Fed could delay its much-anticipated easing cycle, supporting the US dollar (USD). This week, the US will release CPI and PPI data, which, if higher than expected, will likely support the greenback further. With the USD to remain strong, oil is therefore up against a financial headwind. Second, crude oil demand is hamstrung by weak refining margins in Europe. Finally, the bearish reaction to OPEC last week flushed some fickle length out of crude futures and left many bearish-positioned players.

On Friday, the USD surged after the economy added significantly more jobs than expected in May, with nonfarm payrolls increasing by 272,000. This raised speculation that the Fed might delay its anticipated easing cycle. The 2-year US yields rose by 16%, and the dollar index rose by 0.8% to 104.91, its highest gain since 10 April. The robust jobs report has tempered expectations for Fed rate cuts this year. This week, the US will release CPI and PPI data, which will unavoidably come to bear on the USD alongside a slew of elections across Europe over the summer.

Refinery margins, which drive crude demand, remain weak. The Onyx European M1 refinery margin fell by $0.36/bbl in the week to 7 June. Seasonally higher summer demand that was somewhat taken for granted by the market appears on shakier ground in our opinion. This is reflected in European gasoline (EBOB), where market participants are risk-off, awaiting a genuine demand signal following the bearish US EIA data last week – which showed a rise in stocks in excess of 2 mb. In terms of price structure, the front EBOB spread (Jul/Aug) fell from $8.75/mt on 3 June to $5.75/mt on 10 June.

CTA positioning has been a significant driver of flat price direction recently. Commitment of trader data for the week ending 4 June revealed an all-time low in the net speculative length in Brent, matching the lows in flat prices. However, in our view, real positioning is probably less net short as the lows in price were bought into. Onyx’s proprietary CTA positioning model shows that the net positioning of CTA players is very short, indicative of short-side saturation, which in turn lends itself to quick reversals should bullish news hit the headlines.