Why Are European Margins Higher in Asia?

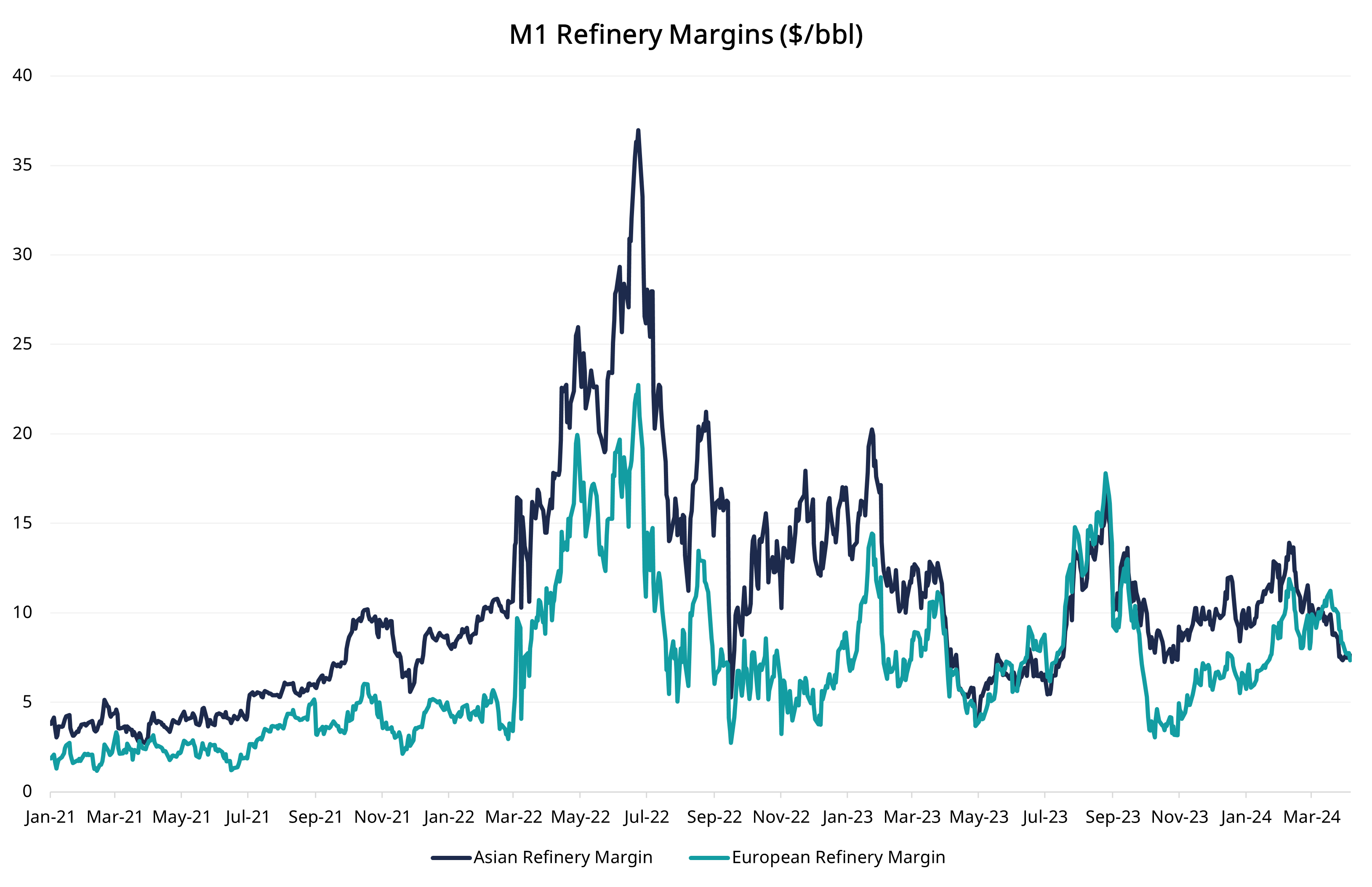

At the end of February, M1 refinery margins weakened in both Asia and Europe, with the former declining from around $11.30/bbl on Feb 12 to nearly $9.65/bbl come Feb 28, whilst their European counterparts came off from $11.30/bbl to $8/bbl in the same period. While both refinery margins climbed up from this point, M1 refinery margins in Europe surpassed Asian margins for the first time since August 2023.

Before we continue, let’s take a quick refresher: refinery margins calculate a refiner’s profit margins. The simplest way to calculate these would be to take the difference between the price a refiner receives for a refined oil product, such as gasoline, jet fuel or LPG, and the crude bought by the refiner to produce said refined oil product. Historically, Asian refinery margins tend to dominate their European peers, and a critical reason for this is the disparity between sweet and sour crude.

Cracking Up

The cost of crude dampens a refiner’s profits and thus impacts their margins. Asian refineries use the Middle Eastern Dubai crude benchmark in their calculations whereas European refiners utilise the North Sea Brent crude benchmark. The difference between these benchmarks is that Brent is a sweeter and lighter grade of crude relative to Dubai, and thus tends to be a pricier benchmark to use.

Lighter grades of crude contain higher proportions of light hydrocarbons, making them yield higher proportions of lighter distillates such as gasoline, naphtha and LPG – all of which are more valuable than heavier distillates such as gasoil which tend to be produced in higher proportions through heavier crude grades such as Dubai. In addition, Dubai is a more sulfur-dense “sour” grade of crude. Sulfur compounds in crude oil can form impurities during refining processes and can degrade the quality of refined products. Moreover, refining sour crude tends to be more complex and expensive relative to the simpler, more efficient sweet crude. Given this, Brent has historically seen better demand and has warranted higher prices relative to Dubai. Given this, crude prices historically dampen European refinery margins more than Asian refinery margins.

OPEC Cuts (Through Asia’s Refinery Margin)

So, what has changed now? Let’s paint a picture: it’s 2020, the world is in a pandemic and no one wants oil. The M2 Brent futures contract slumped from over $50/bbl at the beginning of March to $26/bbl by the end of the month. Two years later, oil markets were shocked once again in the aftermath of Russia’s invasion of Ukraine, which took the M2 futures to $120/bbl in March 2022.

With such volatility in oil prices, producer group OPEC+ announced a 2mbbls/day cut in oil supply in October 2022– effectively pulling out 2% of global oil supplies. OPEC+ reportedly announced the cut to counter rising interest rates in the West and a weakening global economy. In 2023, OPEC+ announced additional cuts in April and June – extending their oil output cuts to 3.66mbbls/day, or about 5% of daily global demand until the end of 2024.

While this sudden tightening of crude sent oil prices rallying irrespective of their grade, it had a more prominent impact on sour crude, adding pressure to the Brent/Dubai sweet/sour crude differential.

This rise in Dubai crude thus softened Asian refinery margins – narrowing down the gap between Asian and European margins. Asian margins ultimately fell below European margins in May 2023 and constantly oscillated around similar levels until September 2023, a time when Brent rallied to the $95/bbl handles.

Moving forward to March 2024, Brent/Dubai witnessed another substantial sell-off throughout the month after a more rangebound February amid a sharp rally in Dubai spreads – which may have once again pressured the Asian refinery margin.

A Poor Month for Asian Gasoil

However, added pressure to Asian refinery margins likely emerged out of the acute weakness across the middle distillates complex in March. Due to the dichotomy between sweet and sour crude and the refined products they yield, Asian margins give a slightly heavier weight to middle distillates like gasoil while European margins tend to do the same with the lighter gasoline. While strength in the gasoline complex buoyed up European margins more than it did Asian margins over March, the Asian gasoil market was battered throughout the month due to a supply glut and lacklustre demand in the region.

What Now?

Looking into April, Brent and Dubai have recorded tremendous bullishness and have crossed into the hallowed $90/bbl region – pressuring margins from both geographies. Interestingly, however, we also see support for the M1 Brent/Dubai and witnessed a rally in the Asian middle distillates complex into the new month. Both these factors would support M1 Asian refinery margins, which are now threatening to once again rise above European margins. However, with a still-tight sour crude complex, and anticipated strength in EBOB, Sing 92, and the NWE Jet and kero contracts amid the amid the upcoming summer travel season, whether these margins widen or not will be something to watch.