In the second week of April, the Asian High Sulfur Fuel Oil (HSFO) complex began an impressive rally. We initially saw support materialise from a weaker European HSFO and ultimately found further strength stemming from players aggressively buying 380 spreads along with the 380 East/West, the differential between the Sing 380 and European HSFO barges. The Jun 380 E/W, on the back of this buying,

inched up from $5.25/mt on Apr 10 to over $25/mt come May 17. While we still see significant buying in 380 spreads and cracks lift the complex, the increased sell-side resistance at these highs poses the question: is the 380 E/W flying too close to the sun?

A Tale of One High Sulfur Fuel Oil

While the Sing 380 fuel oil has shown little indication of a reversal, its European counterpart has seen limited luck. The Jun/Jul 3.5% barges also climbed initially – with the bulls inspired by Asian HSFO’s incredible strength. Prices for the spread edged up from -$1.50/mt on Apr 15 to an intraday high of $3.75/mt on May 01. However, into the new month, the spread cratered to -$3/mt come May 16 amid sell-side traction because of a weak physical. Flow-wise, the Jun 3.5% barge crack also noted over 1mbbls of trade house selling in the week to May 15.

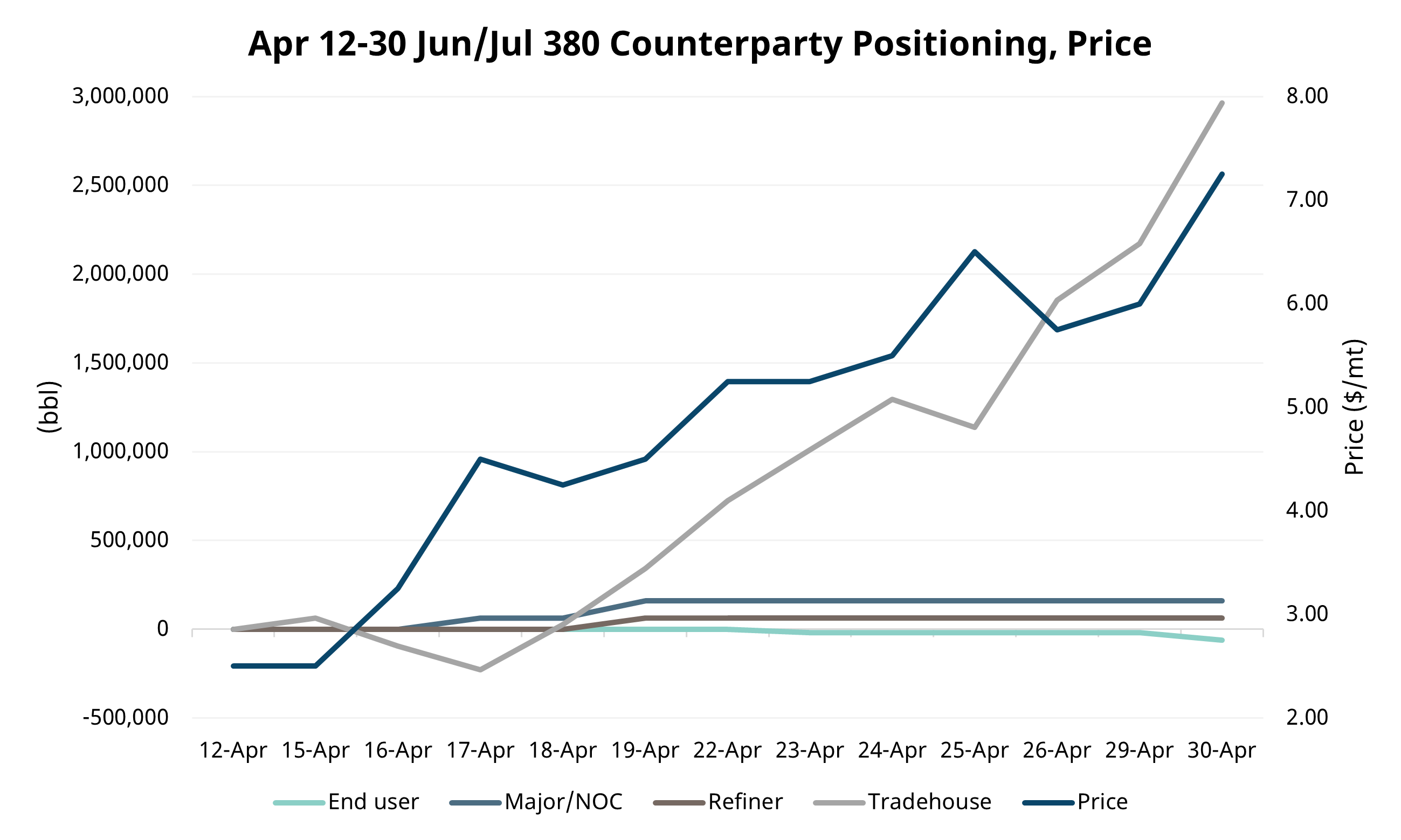

So why is the Sing 380 market so well bid? Fundamentally, we see a tighter supply of HSFO in both Europe and Asia. In addition, while Europe continues to battle tepid demand, Asia has seen comparatively stable bunker demand. We saw physical players buy up Q3’24 380 E/W contracts, perhaps amid expectations of better seasonal power generation demand. Specifically in the 380 contract, we saw a bull run propel up the contract with trade houses buying nearly 3mbbls of the Jun/Jul 380 spread from Onyx between Apr 12 and Apr 30. We further saw 160kbbls of major/NOC buying in this period whilst noting only 60kbbls of end-user selling. In turn, market makers selling the 380 spreads would buy up the prompt 380 E/W contract – implying further support for the 380 complex.

This buying then got a ramp-up following a sell-off in crude at the beginning of May. Perhaps because of its high sulfuric content, HSFO tends to be more driven by crude. Thus, with the July Brent futures falling $3 to the $83.50/bbl handles on May 01 after a bearish EIA announcement of a 7.2mbbls build in US crude oil inventories, we saw participants buying over 1.2mbbls of the Jun 380 flat price in addition to keeping spreads and cracks well bid, perhaps to protect their 380 length. Coupling this with the aforementioned weakness in Europe, the Jun 380 E/W rallied from $12/mt on May 01 to $24.50/mt on May 16 whereas the Jun/Jul 380 spread strengthened from $7/mt to $8.25/mt in the same time.

Future Expectations

The 380 E/W now sits on a 7-day market trading split of 15:85 long:short with trade houses now seen selling 1.2mbbls of the Jun contract in the week to May 15. While Jun 380 cracks continue to be well bid, they too see more sell-side resistance with Onyx’s traders seeing over 95kbbls of the contract sold this week. Finally, we also recorded over 1.6mbbls of selling in the Jun/Jul 380 spread by trade houses.

In addition, we see a potentially bearish fundamental outlook brew in the Asian HSFO market. Complex refineries add “cokers” to them, which allows them to remove their HSFO stream to make upgraded refined products such as gasoline and diesel. However, margins from Singaporean coking units have recently been on a downward trend and have breached into the sub-zero territory – highlighting that it is no longer profitable for these refineries to convert HSFO to lighter products, which may in turn lead them to sell the fuel as it is and loosen supply-side fundamentals.

Finally, further bearish data comes from the UAE. Despite stockpiles of oil products at the Port of Fujairah dropping to a two-month low on May 13, inventories of heavy distillates used for power generation and ship fuel rose 4.8% to 9.963mbbls – a three-week high. Thus, while we continue to anticipate bullish tides for the 380 E/W in the near term given the abysmal performance in European HSFO and still-continued bull run in the Sing 380 complex, the increasing sell side resistance alongside weaker coking margins generate fears that the laws of gravity may be underway for the Asian high sulfur fuel oil.