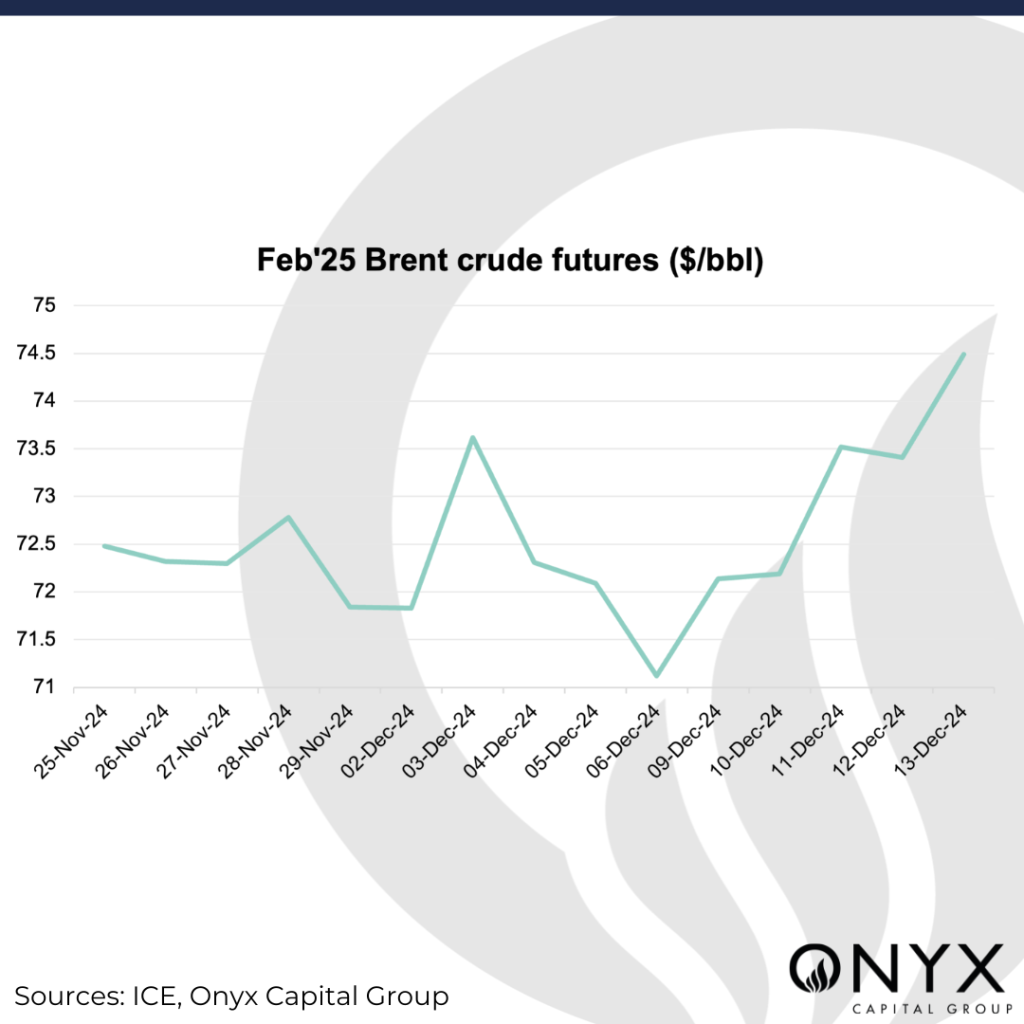

The front-month (Feb’25) Brent futures contract has seen a supportive performance in the past week, rising to highs of $74.50/bbl on 13 December – but has come off to the $74/bbl level on 16 December (time of writing). This week, we anticipate price action to correct lower to the $71–73/bbl level as the market evaluates the following factors:

- FOMC meeting and the impact on the US dollar

- China’s economic uncertainty

- Market positioning

Market participants are awaiting the outcome of the FOMC meeting on 18 December and are pricing in a cut of 25bps. However, the outlook for 2025 remains uncertain as the Fed is expected to take a less dovish approach to rate cuts on fears that Trump’s policies will stoke higher inflation. The December FT-Chicago Booth poll surveyed academic economists and revealed that most expect federal fund rates to hover at 3.5% or higher by the end of 2025. This contrasts with the September survey, in which most respondents said it would fall below 3.5%. Last week, the European Central Bank (ECB), the Swiss National Bank (SNB), and the Bank of Canada (BoC) all cut interest rates, contributing to the rise in the US Dollar Index. In addition, the Chinese Yuan slid following a report that Beijing might allow the currency to depreciate. The fears surrounding Trump’s trade restrictions should support the dollar, which may pressure dollar-denominated risk assets like oil.

Following a weekend of mixed economic data, China’s economic uncertainty should continue to weigh on the oil market. While its industrial output growth of 5.4% y/y in November exceeded market estimates, its retail sales rose by just 3% y/y, slowing from 4.8% in the previous month and below market expectations of a 4.6% gain. The mixed data underscores China’s economic recovery challenges, especially with the incoming Trump administration’s looming threat of trade tariffs. There is added pressure on policymakers to promote consumer-focused stimulus – which follows last week’s Central Economic Work Conference, where the meeting report pledged to boost domestic demand as the first out of nine strategic priorities for the year ahead.

Finally, market positioning suggests that bullish positions in Brent futures are overcrowded, and that potential profit-taking flow might pressure price action downwards. The latest ICE COT data shows an increase in money manager net positioning, with the long:short ratio rising to 2.90:1.00, the highest level since July. With the increased geopolitical risk premia priced in from the recent rally, Brent has seen resistance below $75/bbl as traders turn their attention toward global economic uncertainty. Going into the festive period and without further bullish catalysts, we anticipate price action to consolidate and weaken as bullish money managers take profit amid conditions of lower liquidity. Nonetheless, we think Brent will remain supported above $71/bbl on a tighter market as OPEC+ delays their output hikes.