The Jan’25 Brent futures contract concluded last week on a solid note, closing at $75.20/bbl on 22 Nov off the back of escalating tension around the Ukraine war. Prices softened to $74.35/bbl this morning, where they found support briefly, but fell further to $73.80/bbl at the time of writing. In our opinion, the market will continue to lack direction, and we expect front-month Brent to trade in a range of $72-75/bbl by the end of this week. Critical drivers of oil prices this week include:

US data ahead of seasonally low liquidity

Brent hits a technical resistance level

Mixed developments in geopolitical tensions

US liquidity is expected to dry up this week with the upcoming Thanksgiving holiday on Thursday. Amid these dissipating volumes in financial markets, the US will prepare for key data announcements due this week. Key data releases include Tuesday’s Fed FOMC minutes and Wednesday’s US Q3’24 GDP and October PCE inflation report. The market will look towards the minutes from the FOMC meeting earlier this month for clues on the pace of rate cuts. In addition, October’s core inflation print is expected to come at +0.3% m/m (+2.8% y/y), in line with last month’s increase. Incidentally, this will be the last inflation reading under a Biden administration. While we see stable Brent following the release of data, we caution against headline-driven sharp moves during the Thanksgiving period when liquidity and volumes are very low.

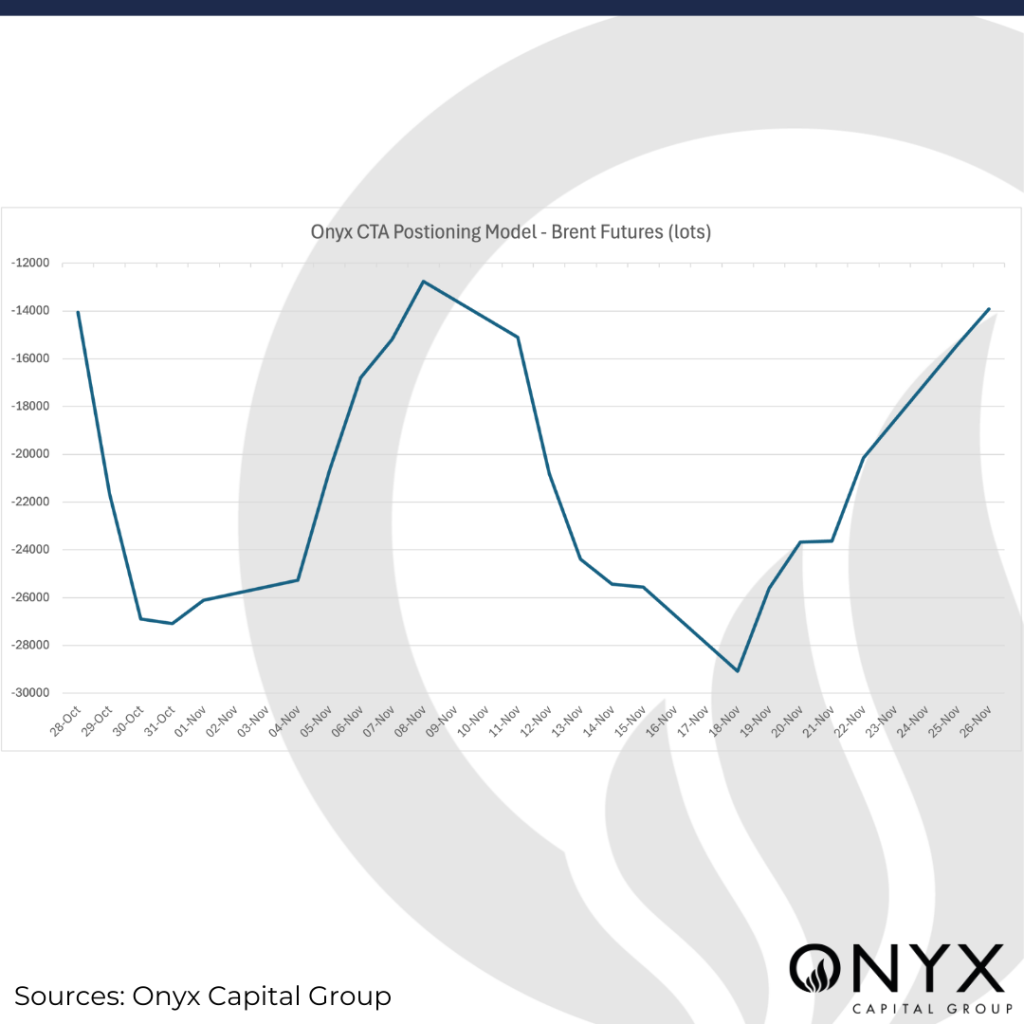

In the past month, we have yet to see the Brent futures contract breach the circa $76.24/bbl resistance against which it failed to move above towards the end of October and in early November. Positioning data dovetails with the recent price action. CTA positioning, as estimated by Onyx, saw a nearly 35% increase w/w in Brent futures to -15k lots on 24 Nov. Such increments have, in the recent past, been followed by retreats and deleveraging. We expect this pattern to continue in the short term, given weak macroeconomic realities.

Finally, the geopolitical landscape is changing. The conflict in Ukraine is garnering greater attention, while developments in the Middle East appear to diffuse. Ahead of its 1000th day, the conflict between Russia and Ukraine escalated following President Joe Biden’s decision to permit Ukraine to use US-made long-range missiles to attack Russia for the first time, followed by the UK and France’s decision to allow their missiles to be used in the war. Russia retaliated by using hypersonic missiles against Ukraine for the first time. The US and UK have imposed additional sanctions on Russia, adding to the geopolitical risk premier supporting oil prices. By contrast, in the Middle East, Israel has reportedly agreed “in principle” to a ceasefire with Hezbollah in Lebanon but is yet to finalise any agreement. A ceasefire may relax some of the geopolitical risk premia supporting oil prices.