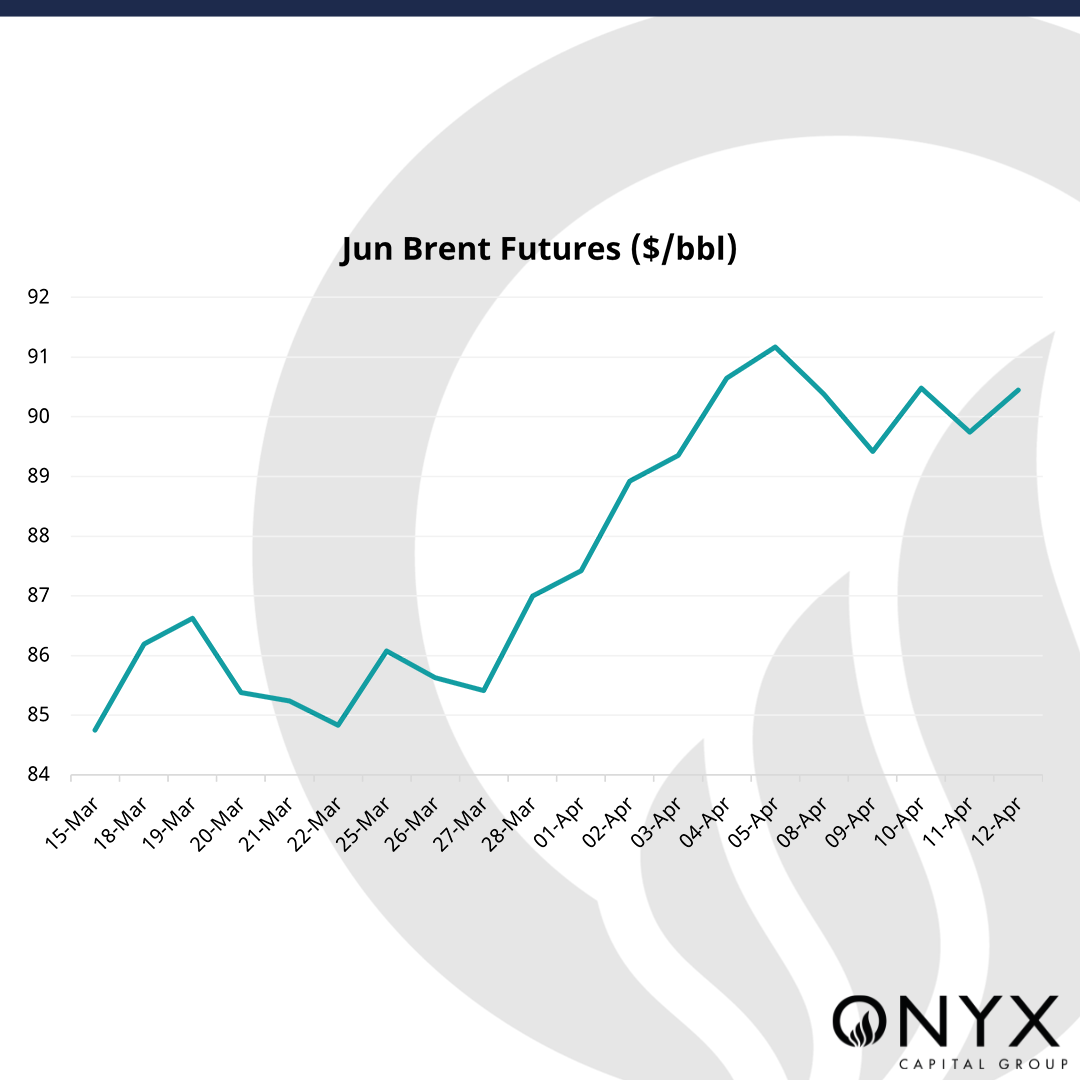

After a relatively rangebound week, with Jun Brent futures oscillating around the $90/bbl mark and hitting highs of $92.18/bbl on Apr 12, Brent futures has opened weaker following the weekend’s events – retracing to below the $90/bbl mark.

The news this weekend was dominated by the conflict in the Middle East. On Saturday, dozens of Iranian drones were launched as a direct attack against Israel, in retaliation for the Israeli attack on the Iranian consulate building in Damascus on Apr 01. Moreover, Iran’s Defence Ministry has threatened to strike any country that opens its airspace or territory to Israel for a retaliatory attack. So the question this week is what will be Israel’s next move? G7 leaders expressed on Sunday their full support to Israel and reaffirmed their commitment towards Israel’s security, and President Biden urged Israel to take a measured approach. Nonetheless, Israeli Prime Minister Benjamin Netanyahu’s war cabinet reportedly favours a retaliation against Iran for its mass drone and missile attack but is divided over the timing and scale of any such response and is yet to make a final decision with further discussions expected this week.

In regards to the oil market, Brent flat price is trading below the Apr 12 close, as participants dialled back risk premiums on the back of the attack – causing little serious damage and being very much choregraphed, formulating an underwhelming response. This muted reaction also highlights low volatility in the market, which is unusual in times of geopolitical tension, as players perhaps adopt a more “wait and see” attitude. Another significant worry is the seizure of a container ship by Iran in the Strait of Hormuz – threatening trade lanes of the strait – through which currently 17% of global oil production flows. It will be important to monitor freight markets as a barometer for how spooked the market is during the opening days of the week.

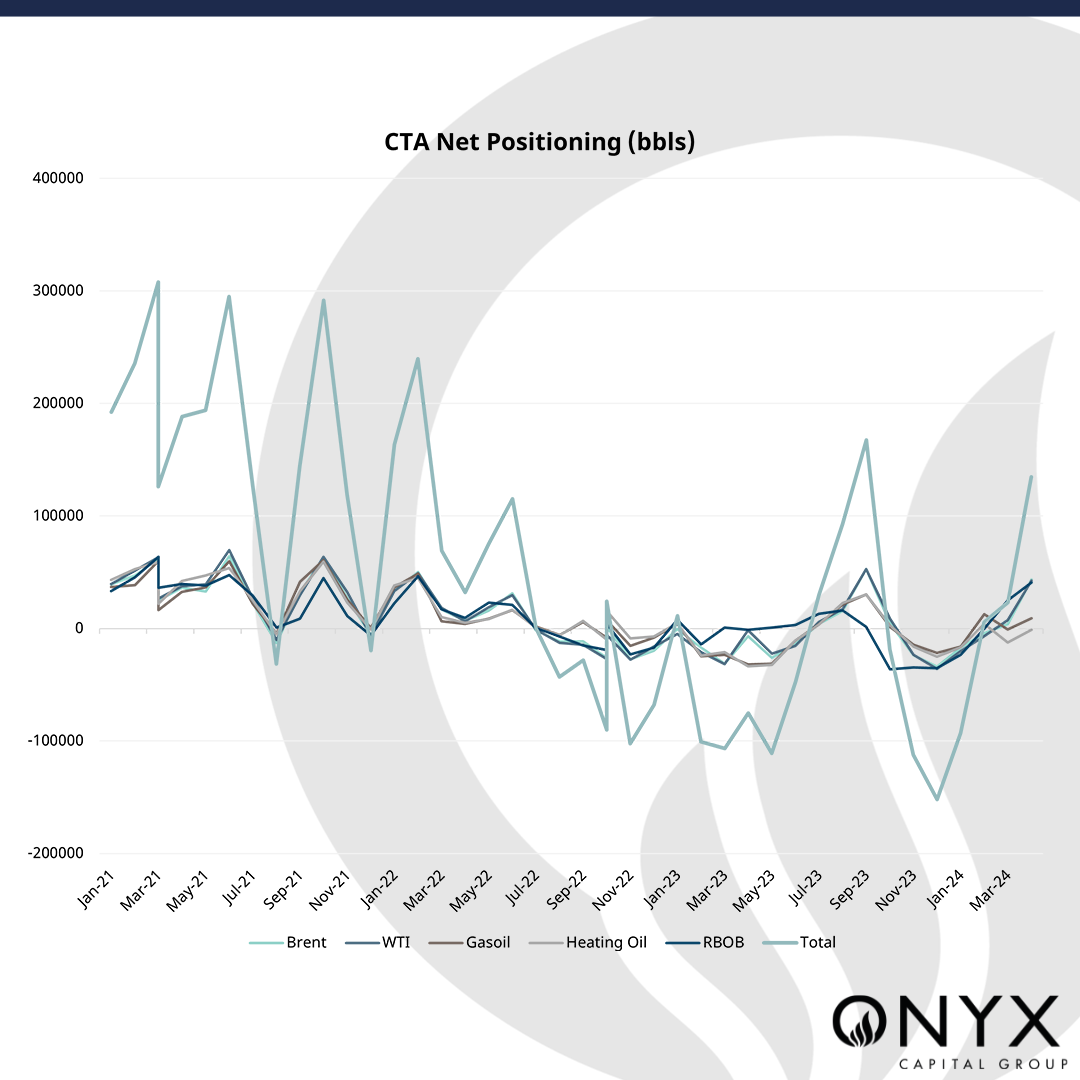

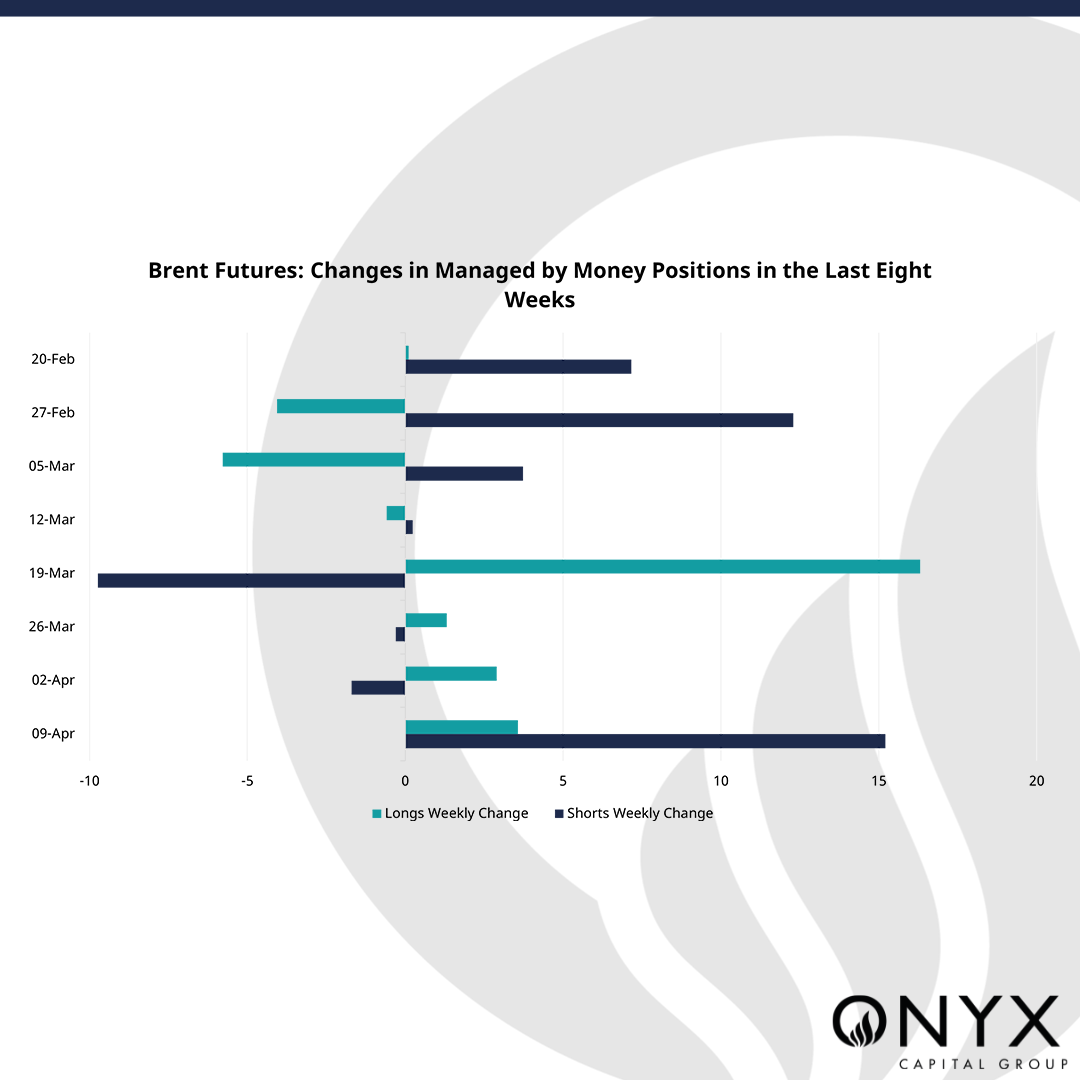

In addition, the market is positioned very long, on both a CTA and managed by money basis. In CTA’s, Brent and total positioning reached a peak of 43.5kbbls and 135kbbls on Apr 08, respectively. Yet, they have since started to tick downwards – printing at 38kbbls and 104kbbls by the end of the week, potentially signalling algorithmic selling and the idea that the market believes it might have to get shorter before rallying once again. Looking at CFTC data for the week to Apr 09, speculative players in Brent adopted a more risk-on approach, with longs and shorts increasing by 13.4mbbls (+3.6%) and 10.8mbbls (15.2%) week-on-week. This has driven net positioning even higher to above +305mbbls, the greatest value seen since Sep’21. In turn, with the almost two week delayed response from Iran, the market may have demonstrated a textbook example of buying the rumour and selling the fact, with the response not forceful enough to twist the markets hand and react with proper conviction.

Looking ahead to this week, we forecast a correction downwards in the market as the debate of how Israel will respond rages on and the current risk premium looks mostly priced in. With this in mind, we hold a cautiously bearish view and forecast Brent prices to print between $86-88/bbl, whilst keeping a keen eye for any signals of a notable retaliation from Israel, as well as interruptions to oil flows through the Strait of Hormuz. The apparent lack of macro money rushing in as of yet leaves the contract primed if there is a bullish headline on the horizon.